We always crave to genrate the handsome returns on our investments, though the market returns are always cyclical. It is always said that do not try to time the market but try to spend time in the market by staying invested for longer time period. We have earlier discussed that a small change in portfolio asset allocation can help you reduce risk for comparable/better returns in Benefits of Dynamic Asset Allocation and How to use a simple Value Index to increase your probability of positive returns. Today, we will try to see if we can utilize VIX to generate better returns on our equity investments.

Understanding the VIX: Volatility Index popularly known as VIX, is deem to be one of the sophisticated tools used by large institutional investors or sophisticated investors. It is a measure of implied volatility of Nifty 50 index options over coming 30 days. It reflects the investors fear in the present market situation. In simple term, VIX signifies the speed & magnitude of changes in Index value. Main reason, Investors go for VIX as it is touted as a great hedging tool due to its negative correlation with the actual Index returns.

| If you expect Nifty to fall suddenly due to some external events, long VIX position can hedge against loses as well as generate significant gains. |

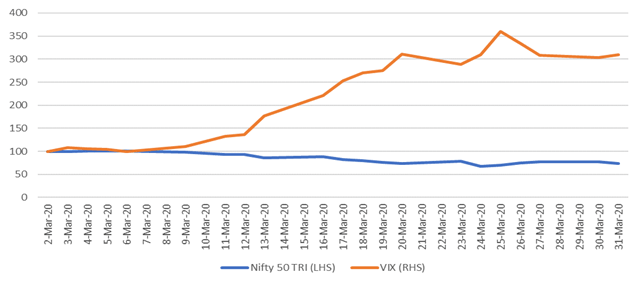

In the month of Mar 2020, index has seen the sharp corrections people invested in Index on Mar 1, 2020 had lost 25%+ by the end of Month. This was a ferocious move and many new punters are still pulling their hair after seeing this much loss. In the same month, If the person would have invested into the VIX then he would have tripled his money by the end of the Month. This relationship of negative correlation also holds for the whole history of 11years (-0.5).

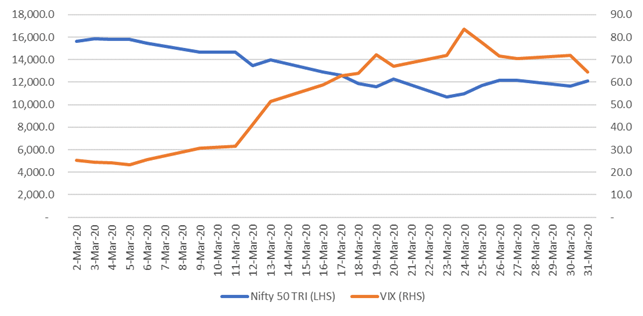

Chart 1: shows the actual value of Nifty 50 TRI and India VIX. The Nifty 50 TRI moved from 15,632 to 12,105 in the month of March, while the VIX has moved up from 25.2 to 64.4 in the same month.

Chart 2: The Comparative value of investments as Base 100

Before you get too excited and think that this is a great way to make money, let me stop you here and show the long-term chart of VIX. VIX was launched in India in March 2009 and over last 11+ years of History, it has been hovering around its Median value of 17.3.

VIX Positions are only useful for short term trading up to 30 days. In long run, VIX reverts to its mean (~17) & oscillates around it.

Interpretation of VIX: If the VIX value is 20, it is expected that over next 1 year the Nifty value would stay within the range of +/- 20%. Though Nifty in itself is a measure of implied 30 days (1-month) volatility, therefore to get the range of Nifty over next 1-month period is calculated using VIX/SQRT (12). For e.g. If the Nifty value is 15,000 and VIX is 20, The Nifty should stay in the range of 14,100 to 15,900. This is a useful information for traders as option expiry nears and Nifty trades outside the expected zones, one can expect them to write (sell/ short) the options in above or below the expected range to collect premiums. Though, I am not a trader so it is of no use to me.

Let’s start with the basic premise that when the VIX increases suddenly, due to its negative correlation with index, Index would have seen the sudden correction. Does it mean that the Nifty investing would have yielded better returns? There have been three main incidents when Nifty VIX have suddenly moved above 35 in last 11 years history, the forward returns appear to be as below.

| Month | 1yr Forward Returns | 3yr Forward Returns | 5yr Forward Returns |

| Jul-09 | 26.4% | 9.1% | 13.3% |

| Sep-11 | 12.1% | 20.1% | 13.8% |

| May-14 | 20.9% | 12.6% | 13.2% |

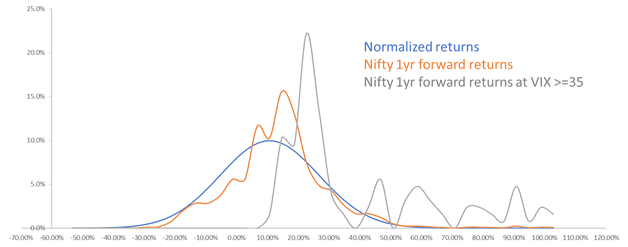

Even though all three returns scenario are yielding in positive and significant returns, this can not be used as a significant basis to gain better return or expected to stay true for future. Though Let’s try to analyse the return profile of nifty returns. Below chart highlights three distributions:

- Blue line is a theoretical normal distribution of returns around mean with equal probability of returns more than or less than mean

- Amber line is the actual 1 year forward return, which has higher probability to get average returns (height of amber line more than blue line) as well as small chance of positive returns like 100% (Long right tail)

- Grey line is the line of importance for us plotting returns, when VIX has been >=35. The returns distribution shifted right, which means that the chances of negative returns reduces and chances of large positive returns are increased accordingly. The geometric mean shifts to whopping 35% with Median returns of ~25%

Few caveats befor you stick to this as a sure shot way:

- The number of observations with VIX >=35 are limited (only 165 out of 2773 observations)

- The history is limited for VIX only to 11 years so less number of business cycles to make any firm view

- Only 6% times VIX goes above 35, you should use this to top up your holdings instead of only investing in periods of VIX>35, As the rule one stays true time in market is more important than timing the market

Assuming the large correction has taken place when VIX increases drastically so further correction is less expected. This might give you large volatile returns in short run so make sure that your overall asset allocation still sticks to your risk profile. Happy Investing!