With every increasing interaction with people, I come to realize that I have a “False Consensus Bias”. I have always assumed that what we learned in college/ school is something everyone knows and applies, It is not true!. A good majority of investors do not understand basic terms like volatility, difference between arithmetic/ geometric mean etc. Still, I am taking a plunge to start with one of the foundation concept in portfolio management “Modern Portfolio Theory” (There is nothing modern about it now, as this theory was first published in 1952.). It is relatively important to understand it’s basic premise and it’s applications can help you build a robust portfolio with little effort. Let’s start with few terms, which we need to understand before hand.

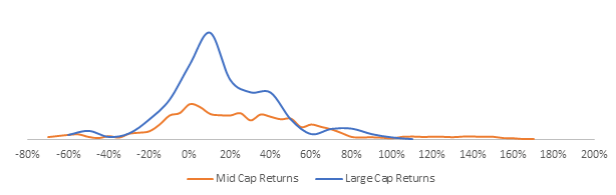

Risk/ Volatility (Variance/ Standard Deviation): Most of us might have heard that equity is a risky investment but only few of you can explain that “Equity is risky because of the wider range of returns possible and it is impossible to tell you the exact return for future.” Among two investment options; The option with wider range of possible returns vs other, will be called riskier. So, Can you tell from the below chart of return distribution that between Large-cap and Mid-cap index, which is more risky & why? (Please answer in comment section.)

In statistical terms, it is measured using the variance or standard deviation of the returns. Higher the variance/ standard deviation, Riskier the investment.

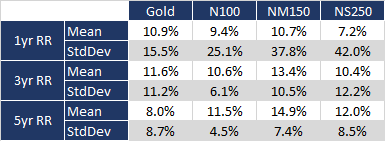

Expected Returns (Mean/ Median): As Equity do not have a fixed return like our fixed deposits, we do get the range of returns as mentioned earlier and shown in above chart. Though, for our simple mind of common investor, we want to understand one return value as expected from the investment. This is roughly represented by geometric mean of the historical returns or median value. For our exercise, I have taken the geometric mean of the (rolling) returns for the period Mar 2007 – Sep 2019.

Gold returns are of GOLD BEES ETF, N100 is Nifty 100 TRI, NM150 is Nifty Mid-cap 150 TRI and NS250 is Nifty Small cap 250 TRI

You will notice that the (geometric) mean returns of equity indexes N100, NM150 or NS250 increases when we look over a longer time horizon 3 yr or 5 yr at the same time, the volatility (StdDev) decrease. This is why we often suggest that equity is an investment class for longer time horizon. If you look at the return distribution graph for equities for longer horizons you will notice that it’s range of returns keeps on shrinking.

Risk Averse Investor: In reality, we all should be behaving like a risk averse investor. Risk averse investor means that an investor should not opt for risky investments unless he gets an additional returns. For example: if i suggest 8% returns in equity (which is volatile/ risky) vs 8% return on a fixed deposit in a credible bank. A risk averse investor should always opt for fixed deposit. “This is why people have fed you with the notions that equity gives you a higher return over long period.” or “You can expect 12% or 15% or 20% returns on your equity investments etc.” Obviously the degree of being risk-averse will change from a person to person, hence one need to invest as per his risk appetite and risk capacity.

As per Modern Portfolio Theory (MPT), in simple terms, as an investor we should invest in an asset or portfolio which gives us the maximum expected return for a given level of risk (StdDev). In other terms, we should invest in a portfolio for a return which is least risky. for example: If i am looking at the 5yr rolling return Mean returns & risk. I will prefer to invest in Nifty Mid-cap 150 (NM150) vs Nifty Small cap 250 (NS250) because mid-caps have higher mean returns as well as lower standard deviations. Also, you can calculate the return per unit of risk to compare the portfolio and pick the portfolio with highest return per unit of risk. Among the 4 investments, if we calculate return per unit of risk using 5yr RR, Gold (8% / 8.7% =) 0.92 has the lower return per unit of risk vs Nifty 100 (11.5% / 4.5% =) 2.534 which is highest. This means that we should never pick gold among these 4 options and stick to Large caps to a large extent unless we want returns in excess of 11.5% in our portfolio (Based on the data).

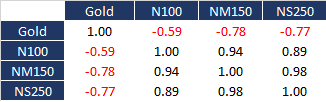

Though MPT does not just stop here, but on the next level suggests that each investment option have a degree of Correlation. (Two investment options can have a similar return cycle, which means that both the assets/ investment option gives you positive return or negative returns, are having +ve correlation. They can have opposite cycle, which means that one of the assets/ investment option gives you negative return and the other have positive returns, and having -ve correlation.) Mixing these negatively correlated assets can reduce the volatility of the portfolio. Below table is the correlation metrics of these 4 investment options, This shows that gold has a negative correlation with all these equity indexes.

I am not going to get into the details of how to calculate the expected return and standard deviation of a portfolio with more than one investment option. Though it is much easier to perform those calculations in excel. Just to test the theory, I made a portfolio of 10% Gold and 90% Equity Nifty 100 TRI using 5yr RR. The expected return comes out to be 11.14% but the standard deviation reduces to 3.6%, which means our returns per unit of risk increases 3.06 vs 2.54 or Nifty 100 TRI alone. We can also find the maximum return per unit of risk in excel using Solver function. The max return/ risk turns out to be 3.9 while taking 29% Gold/ 71% N100, expected return 10.49% with standard deviation of 2.7% only. This at-least confirms one thing in theory that you should not ignore the role of gold in equity portfolio, if not more keep at least 5-10% in your portfolio. You can use the excel to identify the portfolio of your funds mix to get the best sharp ratio, just drop your email id and i will be happy to share the excel with pre-set formula to use. Some basic learning from this exercise:

- Equity investing should be for longer time horizons preferably >5yrs

- Large Caps (Nifty 100 TRI) has the best return per unit of risk, If you are happy with 10-12% returns then it is prudent to stay invested in Large Cap oriented funds only

- Small Caps have the poorest return per unit of risk, it is best to avoid them even for longer investment horizons. (You should read more at Should you buy Small Cap funds?)

- Definitely think of adding some gold to your portfolio 5-10% can do wonders in terms of not returns but reducing risk because of it’s negative correlation with equity. (You should also read Gold: To buy or Not to buy!)

This Dhanteras go ahead and buy some gold that glitters either it can be SGBs, Gold ETFs or Gold Funds, actual Gold coins in the decreasing priority. Happy Investing!!

Nifty 100 – can we use nifty 50 + nifty next 50 index funds to create equity portfolio. How about digital gold for gold investments. Should international funds needed for more diversification purpose.

Hi Kalai,

Obviously point discussed is for general approach to investment and person specific advise.

You can choose to take N50 + NN50 or Now available N100 Index funds. Best to get a Multicap Fund which can do wonders.

For Gold as I wrote it’s prudent to start thinking first about Do you need gold for use and in how many years based on that you should pick a SGB then as second option pick the ETF and if you don’t have trading account then pick a Gold Fund.

International funds are needed in two scenarios as per me.

1. When your portfolio size is huge >100k USD

2. When you expect a Foreign currency denominated expenses like kids education or you settling abroad etc

Rest all can be achieved with keeping exposure in India or buy Fund like PPLTE to get minor exposure to international markets as well.

I meant not a person specific advise

Thanks for response. I am planning to buy gold only as investment purpose(Not for consumption ) and be a part of my long term portfolio along with Equity + Debt products. Kuvera is launching new product called Digital gold , like other gold funds,we can buy and sell in their app. I am just thinking of investing digital gold with allocation of 10-15% in overall portfolio.

.

Let’s stick to SGB as no cost but you get 2.5% on top of Gold returns.

Please send me an Excel sheet mentioned in the article.

Thank you.

Can you drop me an email please.

Sir, please send me your excel file..

Please send me the excel sheet.

Can you drop me an email please.