“Collective fear stimulates herd instinct, and tends to produce ferocity towards those who are not regarded as members of the herd.” Bertrand Russel

The announcement by Franklin Templeton on the eve of 23 April, 2020 about winding up their yield oriented 6 debt fund schemes. Total Aum of INR 26,000 Cr (~USD 3.5bn) was locked in these schemes. The investors in these schemes can neither buy or sell into these schemes. All transaction including SIPs/STPs or SWPs have been cancelled. In my investing career, this is first of it’s kind incident. 11 days before the incident, I wrote the article about one of these schemes and had warned about the redemption pressure causing the distress in the fund (Franklin India Ultra short bond fund – is it time to exit?). Though I had not envisioned the dire situation and possibility of fund closures.

There is enough debate/ articles and news posts about the postmortem of the situation. As usual very few people throw the warning shots about these schemes and till couple of years back the CIO Fixed Income for Franklin Templeton was hailed as the Star fund manager generating exceptional returns while managing the risk.

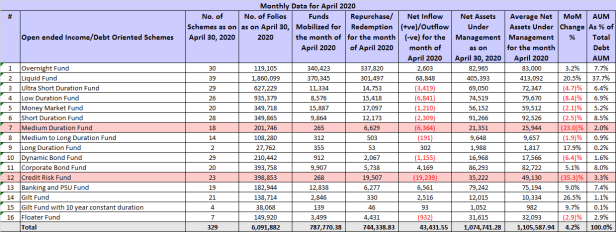

Post this announcement, There has been an immediate risk-off sentiment. It was obvious from the way industry and news put all the blame on the credit risk exposure in funds towards AA/A rated papers, the credit risk funds were brought to the front of this crisis. People dumped their holdings without any considerations or understanding, it was just fear driving from the front seat. 9/16 debt fund categories saw decline in AUM in April vs March 2020.

Credit risk funds lost >35% of their AUM in April month. Though the surprise fall had been in the Medium duration Bond fund category, which has seen the AUM decline of 23% in Apr 2020. Even if both these categories completely shut down, MF industry will come out saying that it is just 5% of Debt funds AUM etc. It will be devastating for the people investing in these funds and have large exposures (Including myself). There are some funds, which has lost upto 37% of AUM within last 2 weeks. This is quite concerning and should be watched out for.

This is one of my favourite category and it has helped me earn ~9% XIRR returns over the last 5 years of investment period in debt funds. let me explain what this fund category is and how it is beneficial for general debt MF investing. Medium Term bond funds as prescribed in SEBI guidelines are funds with Maculay duration of 3-4 years. I have written about debt fund portflio building earlier in How to build debt fund portfolio and Historic vs Future Returns. Though it is never enough to explain the investing landscape, let me try with the yield curve for this.

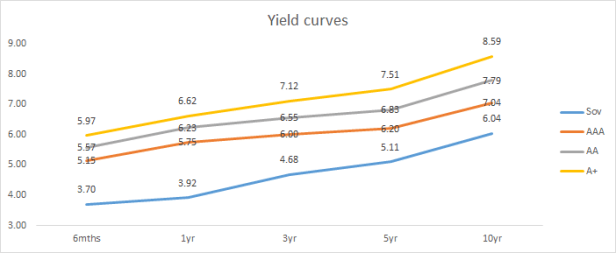

The above chart is for yields as of Apr 23, 2020. The blue line represents the govt bonds of different maturities and how much return one should expect from them on annualized basis. There are two main things to observe and understand:

- You will notice that for shorter duration (6months to 1yr) returns are lower and longer duration (5-10yr) the returns are 1-2% higher. This is what we call duration risk/ interest rate risk. When the interest rate changes the price of bonds change in opposite direction. Higher the duration, larger will be the change. This is one reason why Long term debt funds are more volatile vs short term funds

- The credit risk/ default risk is zero in Sov/Govt bonds, when you take more risk by investing in AAA papers you are roughly getting 1.5% extra returns over a 6 months period. For the higher risk, higher returns you get A+ bonds have 5.97% yield over 3.7 return on Govt bonds

If I am investing in Debt funds (Other than my emergency money), It only make sense for higher tax bracket people to invest for 3yrs+ to get tax benefit due to indexing. It will not be rational to invest in a short duration/ liquid funds and let go your extra yield of 1-1.5% due to duration risk. Also, If your risk profile permits you can opt for schemes with higher exposure to AAA or AA papers for another 1% yield. In normal scenario, I would suggest to invest in funds with >=60% exposure in Sov/AAA or A1+ rated papers. Though in the current risk off sentiment and given Covid situation, hightened risk of credit defaults, one can invest in funds with medium duration and >=85% exposure to Sov/ AAA or A1+ papers.

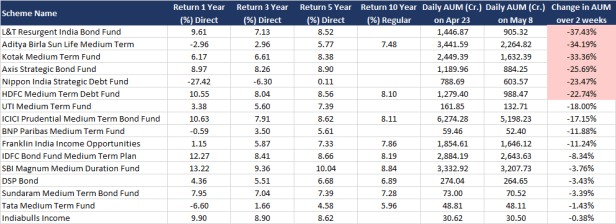

The funds like ABSL Medium Term Bond funds have ~42% exposure towards AA or Below rated papers. Which will increase with the redemption pressure. The fund has a YTM of 16%, this is only reflecting that some of the bonds it is holding are trading at deep discount due to hightened default risk. You should get out of such fund when you can. On the other hand, funds like IDFC Medium term bond which has all holdings of Sov/ AAA or A1+ ratings are having negligible credit risk and can be used for Debt funds investing.

Stay Safe and Happy Investing!