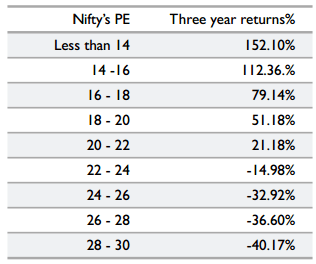

When we saw the sharp correction in July, which is now tagged as worst July in 17 years, lot of people started to point out that the main reason of the same has been the higher valuation levels (It means higher PE Ratios). If that is the case, they should have forewarned us and not analysed it post the corrections. (Though, I did warn about it in Sep 2018 even when I have been on defensive portfolio for almost last 2 years almost.) One of the chart table, which is making rounds on the social media as well as WhatsApp forwards, is the below or similar. This is reflecting that investing on High PE ratio levels end up with negative returns over a 3-year investment horizon, while vice versa is quite profitable. Today we will try to understand if this is still true, if yes then how relevant it is and lastly what should we do to make it more useful for us.

Source: https://craytheon.com/charts/nifty_pe_ratio_pb_value_dividend_yield_chart.php

Is this still relevant?

The short answer will be Yes, but that might not suffice for our understanding.

Recently, PV Sindhu has won the gold medal for the first time in world badminton championship and became first Indian to do so. In the long-standing history of cricket, for the first time England has won the world cup. There are lot of events which proves that if we go just by the historical fact that England has never won the world cup, in that philosophy they should never win as well. Therefore, it is always important to put the statistics and history in perspective. For e.g. how many times the top 5 or top 10 ranked badminton player wins the world championship? Or How many times a favorite cricket team of time has won the world cup? The results would have changed drastically. Still a topple up like 1983 world cup can happen and you can not predict it with surety so always keep your options open.

Can we use PE values & historical returns for investing?

Yes and No, No because the world around us has changed a lot and a simple prediction saying that history will repeat is not good enough. If you look at the recent two changes in the index constituents you will realize that we have replaced HPCL by Britannia and now replacing Indiabulls Housing by Nestle, both these changes will push the PE of index much higher given the higher valuation multiplier to FMCG companies.

Yes, because if history does not repeat itself then it often rhymes. We do not live in the world of past there has been impact of inflation across these years as well as the credit cost has come down drastically.

What valuation data can be used for improved investment returns?

As I mentioned that the world of finance has changed drastically over last 2-3 decades, we are now slowly transitioning into a lower inflation and interest rate regime.

- The cost of credit is a big factor of equity valuation and PE multiples get impacted by the same, so if we have a lower interest rate scenario, we have to adjust the mean PE expected value upwards. I wrote about it in Sep 2018 post in details, please read the same

- To adjust for the inflation impact, we can use the Shiller PE or PE10 but that means you either calculate it at your end or use someone else’s hard work using google

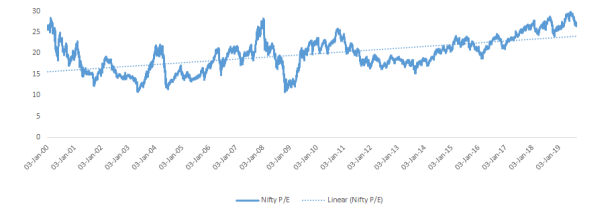

Below is the chart of Nifty PE since Jan 2000 and its trend line moving up from 15 to >20 now.

Though I migrated a bit to a different valuation index which I feel has a better predictive power that just PE standalone. I use a mix of PE & PB valuation levels because we have moved into the landscape with higher PE levels but at the same-time we have become efficient and got lower PB levels. I wrote about its interpretation earlier this year in May 2019, Lessons from Nifty History. Most of this data is available on NSE website to be used or what you can simply do is follow one valuation metrics at the least (other options can be ICICI Pru Valuation Index or Motilal Oswal Valuation Index)

How to interpret & apply the valuations index into investment practice?

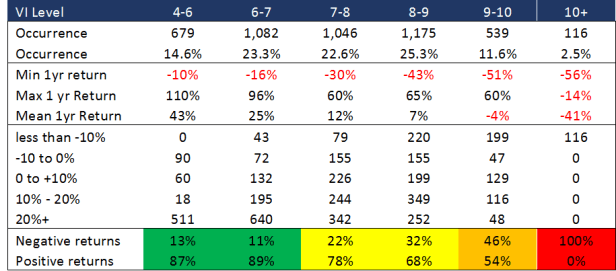

Below is the table which you can use as a reference point and apply on your portfolio, my 2 cents and quick suggestion will be to book profit when it is at 10+, stop new investments in equity if you already have sufficient exposure when it’s between 9-10. Also if it goes to 6-7 or below, buy more equity than your required asset allocation.

Hope this helps to navigate the equity markets in a more secure way than your current situation. To find our recommended funds, Please read Mutual funds.

Keep learning & Happy Investing!!