“We must know what questions to ask & ask them frequently. Have conditions changed in a ways that necessiates a change in strategy?” – Gary Kasparov

More you speak with people, more you realize about the various tactics deployed by the sales person to trap the gullible investors. One of the conversation was shared by the friend to me. He was pitched with the idea to invest in a mutual fund to get regular income in form of dividends and on top of it, sales person touted this as a strategy with lower risk. The data presented was from HDFC Balance Advatage fund – Dividend payout scheme. He suggested that “if you have invested INR 10lakhs in the fund on Apr 1, 2019, you would have recieved roughly INR 10,000/- per month as dividend and after the recent market carnage on Mar 31, 2020 you would have held balance of INR 643,804/-. Therefore, total value as INR 769,055/- (643,804 + dividend 125,250) vs INR 747,183/- in a growth option. Benefit of INR 22,000/-“ . Most of the retail investors could not find the problem in this information presentation. Today we will try to work our way to analyze the Growth vs Dividend Payout or Dividend Re-investment scheme and learn to poke hole in such claims. The analysis is done keeping equity mutual funds in mind:

What is the meaning of Growth & Dividend option in a Mutual Fund?

Mutual funds collect/ pool our money and invest in stocks/ shares of various companies. To track our investments we are alloted the number of units in the fund, and the value of investments is tracked in form of Net Assets Value (NAV) of the fund. NAV of the fund changes in accordance with the change in price of stocks/shares fund has bought and dividends it has received.

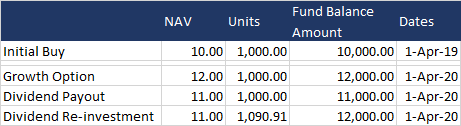

Let’s take an example; If we Invest INR 10,000 in a fund with NAV of INR 10, we will be alloted 1,000 units of the fund. Fund has invested in various stocks and generated 20% return in a year, for dividend option it declares a dividend of INR 1 per unit. How does it reflect in our holding.

- In Growth option, the value of NAV moves up by 20% to become INR 12/- and the value of investment becomes INR 12,000/-

- In Dividend payout/ re-investment option, As the dividend declared is INR 1/- per unit the NAV is adjusted down for this dividend amount & becomes INR 11/-

- In case of dividend payout, you receive INR 1,000/- cash (1,000 units x INR 1/- dividend) and the fund balance remains at the INR 11,000/- (1000 units x INR 11/- NAV)

- In case of dividend re-investment, dividend amount of INR 1000/- is re-invested at the prevailing NAV of INR 11/- and the extra units 90.91 (Dividend 1,000/ NAV 11) are alloted in the portfolio

In theory without considering the tax implications, The output of the investment in the fund stays same irrespective of the option chosen (Growth or Dividend).

Does Dividend option reduce our risk?

Let’s consider two scenarios that after one more year, The fund has generated either a -15% or +15% returns to analyze if their is any advantage in dividend option.

- In Growth option, we will have fund balance of INR 13,800/- (12,000 + 15% of 12,000) or INR 10,200 (12,000 – 15% of 12,000)

- In Dividend payout/ re-investment option, assuming before dividend

- In case of dividend payout, you receive INR 1,000/- cash and fund balance of INR 12,650/- or INR 9,350/-

- In case of dividend re-investment, the fund balance will be INR 13,800/- or INR 10,200

You will notice that the movement of Dividend re-investment is same as Growth option. Though in case dividend payout, our holdings fall less in declining market by INR 150/- vs Growth option (Div fund value 9,350 + Cash 1,000 – Growth fund value 10,200). The difference is merely because of reduced exposure in the fund due to cash payout of the dividend. The fall is less as well as growth is less, therefore the statement that dividend payout option is less risky is wrong.

How does it work in actual world with tax implications?

The dividends are not a tax free source of income, in the financial year FY 2019-20 they were subjected to Dividend distribution tax (DDT) of 11.65% (with surcharge & cess). The tax was deducted at source so it was assumed to be tax free. In the recent budget, the DDT has been abolished and now dividend is part of your taxable income. They are taxed as per your income tax slab, it can taxed at the higher rates of 30% & cess if you are in the highest tax bracket. To understand it’s impact, let’s go back to our original example:

In old tax regime, you were paying the tax on the full dividend amount and it was slowly eating your investments without your knowledge (as below table). In new tax regime, you should be paying the tax on the full dividend amount and it can go as high as 30%. Therefore, It is better to stay with growth option.

At-least my Cash flow is secured, while using dividend option?

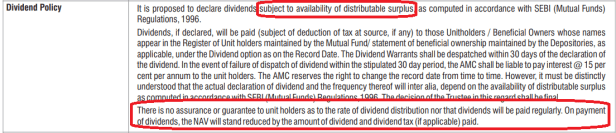

Getting the regular income from the fund has been the main need exploited by sales people, while advising for dividend payout options. You would be surprised to know that 35% of the AUM of Hybrid funds is in Dividend option. As it is assumed that funds will continue to pay the regular dividends as per their recent records. No one reads or understand the Key Infomation Memorandum (KIM), Let me help elaborate the section about dividend policy with below highlights.

- There is no assurance or guarantee about the rate of dividend or if it will be paid regularly. (Don’t be shocked yet)

- It is always subjected to distributable surplus. Distributable surplus is the gain generated if the fund has sold shares at gain or received dividend from thier holding. If there are no gains or Fund sells the holdings in loss, the distributable surpluys can go to zero and no dividends will be paid

- Even if the fund has distributable surplus, the amount of dividend is at the mercy of fund manager/ fund trustees judgement. If the market corrects drastically like Feb-Mar 2020, Portfolio managers can decide to deploy the money in buying stocks at cheaper valuations vs paying out to you as dividend.

In summary, The change in tax lanscape made it pretty clear that one should avoid the dividend option. There is no surity of dividend income and it can not be counted as a regular source of income or a superior risk management. Growth Option will be better to invest and you can schedule a systematic withdrawl plan to generate a cash flow.

Happy Investing!

Do read about my favourite funds across categories: Multi-cap, Large cap, Large & Mid Cap, Aggressive Hybrid fund, Mid cap fund etc.

P.S.: The only exception I can think of, are people in lower income tax bracket of 0-10% as they would have lower tax on their dividend income vs Capital gains tax of Short term 15% & 10% in case of long term gains in excess of INR 100,000. This will also be debatable as full dividend amount will be taxable while in case of growth option only gains will be taxable. Another point to analyse at some later dates.

Exactly…!!!