Let us start with understanding of step 1, Should you invest in a debt fund portfolio?

In a global wealth study for 2017 by BCG, One thing that stands out was the portfolio composition of investors in Asia vs Investors in North America. Asian tend to have 65% of their investments in Cash & deposits vs 14% investment by North American and the figures are reversed for Equity investments 70% for North American vs 23% for Asia. This is due to two main reasons, one is the availability/ reach of debt products in markets in form of deposits by banks & post offices and second is our inherent nature to look for stable and assured returns. If you will collate all your investments, you will be surprised to know that it is true for you that >70-75% of your investments are in Debt products (Savings account, Fixed Deposits, Recurring Deposits, Monthly Saving Schemes, Tax Saving FDs, NSCs, Money back or Endowment Insurance plans, Public Provident Fund, Employee Provident Fund, Sukanya Samridhi Scheme, Senior citizen saving scheme etc.).

Few of these products are really very optimal and suitable to invest in terms of their return and risk profile: Public Provident Fund, Employee Provident Fund, Sukanya Samridhi Scheme, Senior citizen saving scheme, PM Vyay Vandan Yojna. All these have certain limitations as well.

- Except PPF, not everyone can invest in the other schemes unless they fulfill the required criteria

- Liquidity of these investments is limited and restricted by its own clauses

if you can not invest in these options and you fall in tax bracket of >20% tax then best place to get reasonable stable returns are in form of Debt Mutual Funds. Also, If you are Liquidity freak like me then you can also leverage the Debt Mutual Funds along with above options. No need to read further if you do not fall in any of the above two category.

Are there any risk in Debt Mutual Funds?

Nothing comes for free, If Debt Mutual Funds provide you option to get better return and liquidity, It also exposes you to interest rate and counter party risks.

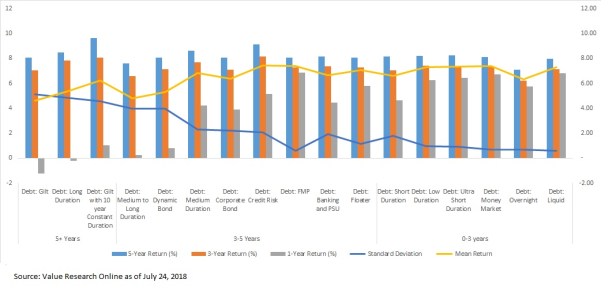

- Interest rate risk: Debt Mutual Funds do not provide predefined returns for the agreed investment horizon like Fixed Deposits. With the change in market driven interest rates, the return of the Debt Mutual Fund changes. If interest rates goes up, the return decreases and vice-versa. The change in return depends on the duration of bonds the fund is holding, means the fund holding 10year maturity bond will see higher change in returns vs fund holding 15 days treasury note. You can see from the below chart that Long duration funds are giving lower 1-year returns vs Liquid funds.

- Counter Party Risk: When the company issuing bonds default on it’s payment of interest or principal due, this is called counter party risk. Government bonds (Gilt’s) are considered to be free from such risk but Corporate bonds do have such risks, which can be mitigated by buying the bonds of only highly rated corporate or can be reduced by diversifying your investment across multiple companies so that default by one should not hamper your portfolio drastically

Which Debt Mutual Fund should i buy?

Chart shows you the recent categories of Debt MFs as per latest SEBI guidelines. When you want to invest for shorter time horizon you should move towards extreme right (Liquid Funds). Investing for decently large emergency corpus or parking money for short time frame should stay in those categories as the mean returns are stable across 1,3 or 5 year periods as well as the Std deviation is smallest for this category.

If you want to invest to get better returns over medium term of 3-5 years period, you can use Medium term plans or Corporate bond funds. People looking to invest for long time horizons for retirement or specific goals like child’s education or marriage can also leverage gilt funds, opportunistically.

Read more on Mutual funds, Retirement Planning.

Please speak to your investment adviser to check the funds suitability for your risk and portfolio requirement.