“You either die hero or live long enough to see yourself become the villain.” – from The Dark Knight

Franklin India Ultra Short Bond fund was launched in Dec 2007 and has a history of 12+ years with return since launch of 8.57%. In the current mayhem in the markets and the series of credit risks events, people have been losing their confidence on the debt funds. I have been personally invested heavily in the bond funds, and FI-USB has been one of the few funds in my portfolio with significant exposure. In the last 7 years of investing in the fund and keeping 8.9%+ return is a pleasing experience, this is partially due to timely reducing exposure by half, before the Vodafone-Idea side pocketing (hit of ~4.4%). Lot of people are invested in this fund and in the recent month, it have given -ve return on 9 out of 20 days. It has obviously caused the concern in investors and they worry about any other credit event. Let’s try to analyse this fund with its historical/ current data to take our call instead of relying solely on emotional response. (Why not emotional response?)

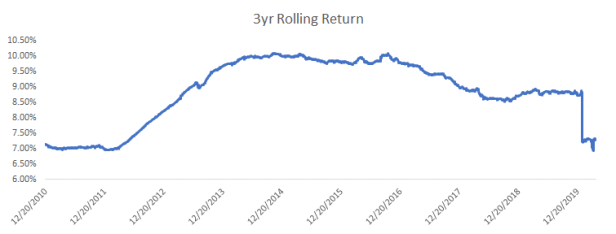

Historical Return Profile

In the last 12+ years history, the fund has given 8.57% of CAGR. I looked at the 3 yr rolling return for various periods as below. The worst return scenario has been 6.94% annual return for 3 yrs (Mar 2017 to Mar 2020) and best has been 10.1% return (Nov 2011 to Nov 2014). The mean as well as median return for this fund has been 8.9%, which is nothing but phenomenal.

Yield to Maturity (YTM)

I have explained in earlier write-ups, why YTM is more important then the historical returns profile (Historical vs Future Returns). The yield to maturity reflects the expected return generated from the current bond investments by the fund over the duration of investments in case of no credit risk event (defaults). The current YTM of the fund is 9.48% for a duration of 0.62 years, this is pretty attractive return from the bond fund.

If you have been a regular reader of my articles, by now you would have realized that I am more concerned about the risk i am taking in my portfolio vs the return I am generating. So let us analyse the risk profile of the fund to make the complete assessment.

Credit risk

This fund has always been more risky then it’s counter-part just by the virtue of taking more credit risk. To understand this in more details, Let’s understand the riskiness of bonds in terms of ratings. As a short term debt fund, our benchmark is Govt Treasury bills which are theoretically risk free. In increasing level of risk below should be the sequence: Sov -> AAA/ A1 -> AA/ A2 -> A/ A3 -> BBB/ A4 -> C or D.

The fund has no exposure/ investments in the Sov and <2% exposure in AAA/ A1 instruments. Majority of the investments are in AA rated bonds ~84% and 22% in A & below rated bonds. Therefore from the fund definitely has a higher credit risk. Most of the bonds are from the NBFCs, which seems more vulnerable in current scenario of lock-down in my non-expert opinion.

Another way to mitigate this risk is to diversify and have lower exposure to a single company or bond. It currently holds 88 different bonds but Top 10 holdings make ~40% and biggest exposure being >7%. if any of these defaults, it will be a big dent again.

Liquidity Risk

What is Liquidity risk? Liquidity is a measure to understand the ability to translate the investments into cash by selling, for e.g. If you have a residential apartment worth 70lakhs, and you have to sell it to generate cash within 10-15 days there is a very high chance you will end up realizing <70lakhs even if you are able to sell it. That is because of lower liquidity of the real-estate market.

Why it is important? The fund has seen the pressure of accelerated redemption over the last 6 months. it has lost half of its AUM from 20,130 Cr in Sep 2019 to 10,964 Cr in Mar 2020. Losing roughly 1,500 Cr every month.

This has taken the toll on the fund as it has to liquidate its more liquid and safe investments in AAA/A1 category. In Sep 2019, it had 27%+ investment in AAA/A1 to <2% in Mar 2020. It means if the fund continue to face the similar level of redemption, it will have to liquidate the AA category bonds, which will be loss making trades in general. The fund is already having -7% cash/ call money investment, which means it had to take a loan/ overdraft to meet the redemption pressure. It is also important to note that fund has ~30% investment in the bonds maturing in 2022 or afterwards.

Re-Investment Risk

If my investment horizon is 3 years and the fund duration is 0.62 years, It means that the funds investment will mature and need to be re-invested. As we seen the RBI has lowered the interest rates, the new investments bonds will also be yielding lower returns if the credit risk is same. This means that the YTM of 9.48% is not sustainable and will move lower.

Interest Rate Risk

This i have covered earlier but in summary if the duration of the fund is higher then the increase in interest rate will be negative for fund profile and vice-versa. Since the Modified duration/ duration is <1yrs, the fund has a lower interest rate sensitivity though higher vs peers in same category.

In Summary, The fund has an attractive return profile but the risk levels are definitely higher.

- If you have a higher risk appetite and the investment in this fund is not your emergency corpus or for short term goals, you can stay invested in the same. Please be vigilant on the redemption pressure, if that continues for few more months, it will be unsustainable.

- If you have invested for short duration, and your goals are due in next 3 yrs or this is your emergency corpus, it will be more prudent to sell and get out of this fund.

- If you have not invested but are thinking to invest in this fund, please re-evaluate your decision. You can read about how to build your debt fund portfolio for more details.

In my humble opinion in current scenario, for additional 1% to 2% returns the risk exposure is not justified. One should size their exposure in this fund accordingly. It’s always better to be safe than sorry, Let me know your assessment.

Happy Investing!

Thanks a lot, I just exited from the fund after reading this article.