“Education is a lifelong journey whose destination expands as you travel.” – Jim Stovall

Every passing year brings in some new found realization of an old wisdom, which provides the joy to our soul. In 2017, I made a commitment to rejuvenate my habit of reading. I committed to finish one book for the year but ended up the finishing 3 books. Now, after 5 years, that commitment has turned into a habit. When I tried recalling the list of books, I was pleasantly surprised that I had finished eight books in the last six months. And it was not the best part, the best part was that I was not making any effort, it just happened naturally. This reminded me the power of habit, “The choice once complicated and tiresome is now default/ automatic.” Same has been true for my investing journey towards financial independence (#FIRE) the retire early was never the goal.

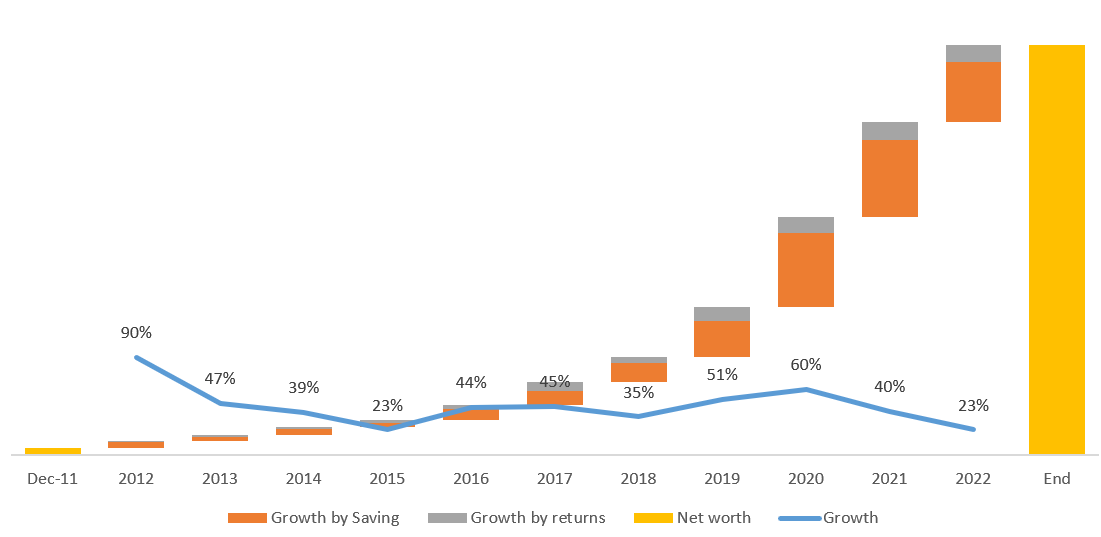

After the 11 year in my journey, at the end of July 22, I have accumulated the corpus equivalent to 46x times the annual expenses. This can safely qualify me as financially independent. For the last four years, the return on portfolio has been higher than my annual expenses sufficiently in each year. This milestone of FI does not mean that I have become a multi-millionaire but it means that compared to my small needs, my corpus is sufficient for my easy survival. The growth of portfolio in these 11 years have been 56x, compounded growth rate of 40%+. This is not the return on my portfolio, The main contribution of this growth comes from the meticulous saving 60% and balance 40% in form of return on portfolio. This should be the reminder that higher income, higher savings rate and lower expenses are they key ingredients of financial independence.

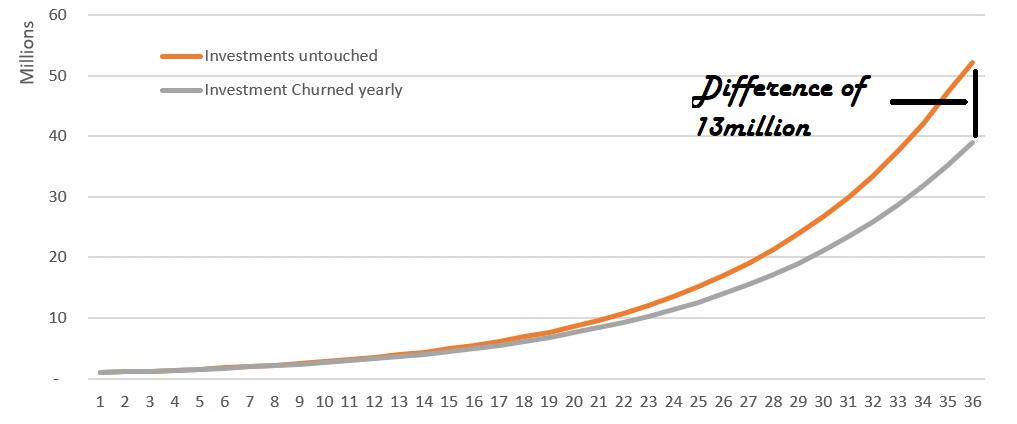

These letter/ blogs have helped me tremendously in my journey to financial independence as it brought the clarity and evolved my understanding of concepts from practical perspective. It keeps on building the new knowledge as I delve into the details. During the last review, I talked about my concern towards higher churning of my portfolio. Now, I am quite clear and have gained conviction that it is way better to have a portfolio without any churn. Even at times additional 1% gain on CAGR due to churning might not be sufficient to mitigate the loss on account of taxes. If two people start the portfolio with 1million (10 Lacs), where 1st person is able to compound the portfolio @12% without any churn and the 2nd person achieve the growth each year but churns it on annual basis. Person 2 would be poorer by 13million (1.3 Crs) compare to Person 1 after an investment horizon of 35 years. This re-emphasizes the importance of being a buy & hold investor in most cases [Read the most critical part of Investment journey].

After this milestone, We would also need to plan for the withdrawal phase, after the long investing period the initial principal amount has multiplied by many times. Due to FIFO method of accounting, the withdrawals would be capital gain intensive and potentially tax in-efficient. If we take an example of a diligent investor who has invested INR 5,000/- per month for 35 years of his career and accumulated a corpus of INR 1.15Cr @8% returns. If he decide to withdraw only 120k in a year {10k per month}, roughly 113k would be the capital gain. Therefore, anything more than 120k would result in an increasing capital gains tax liability. There are ways to optimize that situation and minimize your tax outgo, which we would discuss at another time.

Now most often, I get asked about the secret sauce for achieving Financial Independence. Let me try to summarize few key themes below:

- Get an early start for your investing journey, If you have not started so far then start today. A person who starts saving at age 25 with 8% rate of return on investments can accumulate more corpus than the person starting at age 35 with 10% return on investments both retiring at 60.

- Minimize your tax savings, The money saved from pre-tax income is better than saving from post tax income immediately and the gain compounds. I remembered writing my very first article was on 80C tax savings, in the year I earned taxable income.

- Your asset allocation should align with your goals, don’t go for thumb rules like (100-age) etc. as your goals might be short term like buying a bike/car or down payment for house.

- Be very thoughtful of buying and selling your investments. You don’t want to keep buying and end up di-worsifying your portfolio or selling investments and disrupt the compounding. Once you buy with conviction specially in instruments like Mutual Funds, The most important part is hold onto your investments.

- Understand and Identify the good vs bad costs. Aim to reduce the various bad costs in your portfolio.

Obviously there are many other smaller but important aspects in the journey. Over the last 10+ years, I have written down 100+ articles so far. Most of these articles were the outcome of conversations with friends and thoughts we had went through. Hope you have enjoyed the articles so far, Let me know your queries or topics you want me write about more in future. I would be spending more time striking new conversations, while mapping the next leg of my Investment journey. I am also consolidating the articles related to my own process and decisions made so far under “My Journey” tab. Lastly, don’t forget to subscribe to the blog and hear about the progress on Project Sail (A portfolio with >13% returns over last 45months with lower risk and max draw downs vs other options.).

Happy Investing! Please leave your thoughts in the comment section.