Asset allocation/ Diversification as per Investopedia is “Diversification is a risk management technique that mixes a wide variety of investments within a portfolio.” which can be interpreted in two manner:

- It reduces the risk of portfolio for same level of returns, Or

- for same level of risk, it tries to achieve the best returns possible

Diversification can be across asset classes or can be within the asset class. e.g. you can hold large cap funds, mid or small cap funds with in equity. Right amount of diversification can help you have less volatility in your returns. Diversification can also be called as synonym of asset allocation or in plain terms “Don’t put all your eggs in the same basket”. Just for elaboration, I did not make 60% in CY2017 as I was invested in other asset classes but at the same time in CYTD2018 my returns are still positive in high single digits. Thanks to Asset allocation.

The key point to remember in asset allocation is that the risk (volatility) decreases due to diversification only when the asset classes are not correlated. When you mix a different type of equity asset classes, the benefit will be marginal but putting equity with Debt or Gold will drastically improve your risk adjusted return. This is a simple concept taught in our classes but lot of us fail to implement it or don’t think it in holistic manner.

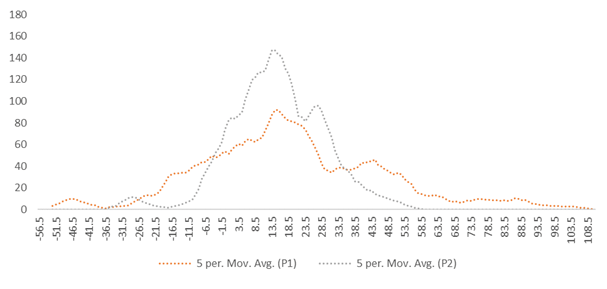

To prove my point in a simpler manner with data, I ran a simulation on NIFTY 50 TRI as index for equity returns and created two portfolios; Portfolio 1 (P1) is invested 100% in equity and Portfolio 2 (P2) invested 50% equity & 50% Debt (@8% annual return). I gathered the data since Jan 2000 to run the simulation with 1 yr forward rolling returns. Below are the results:

- The Average return hovers in the zone of 8.5 to 18.5, What changes is the increased chances to get returns closer to the median value. (Increased height of the P2 plot)

- Your chances to see any extreme positive or negative return decreases in P2

- In P1, there are 26% cases when you will see a -ve 1-year return in your portfolio while in P2 it reduces to 16.6% only

Due to these changes in return profile, your risk & reward profile improves 3x (5.47 vs 1.75). Isn’t it amazing?

Happy Investing!!