During my childhood when I was learning how to ride a bicycle, my brother first taught me how to peddle it and control while he was holding the bicycle with me. When he realized that I can peddle it and control it while being in motion, he suddenly changed his gears by making it difficult for me. He started asking me to mount the bicycle without his support and once I mount successfully, he will often ask me to stop within 10 meters. This was painful as I was young bicycle was taller than me so mounting or getting down was difficult. I often fell in this process but realized that the difficult part in bicycling is keeping control while mounting or getting down. The same was true when I learned driving the car. Surprisingly, its true in flying the plane as well. As per annual Boeing statistics for commercial jets, >60% fatal accidents for a period of 2007-2016 happened either during take offs or landing, Landing had 48% fatal accidents. The reason, I am focusing on the landing, is because in our investment journeys most of us are not investing to keep perpetual investment. We are saving to accumulate money for our retirement, some for financial freedom, others to meet their obligations and very few for wealth maximization. In any case, you should know when to take your money out from an investment. There is enough information on how, when and where to invest but very rarely people talk about when to sell.

There can be many reasons to sell but few main broad categories I came across during my career and personal experience are 1) Requirement to have cash for expenditure, 2) Valuation of the investment, or 3) Tax optimization 4) When you made the wrong investment. Most of the cases I see people sell due to reason 1 & 4 and very few will sell for 2 & 3. Let’s discuss these reasons in little detail to ascertain and identify when is it best to sell your investment.

- Requirement to have cash for expenditure: This could either be a planned expenditure or an emergency expenditure. I often saw people selling their investments due to a later than a former category. Sale executed in haste often ends up being not so profitable, either we do not get the best price or might have to pay an exit load, or it might be tax in-efficient. In such scenarios, when and how should you sell your investments?

- Planned expenditure: This is relatively easy because you can sell your investments in optimal manner. Every year you should try to foresee any big-ticket expenses due in next 2-3 years. Try to hold that money in liquid format or in least volatile format. It will help you to meet your requirement as well as avoid any fluctuations in investment value. Currently if money is in any other asset class (Equity, Real Estate or Gold etc) you should move it to the suggested asset class. Suggestion is to hold this money in FDs/ Savings accounts with sweep-in/out facility, or in liquid funds or in arbitrage funds as well.

- Emergency expenditure: This is the worse reason to sell but in certain circumstances it is un-avoidable. We should try to escape it by planning for emergency corpus as a separate part of your portfolio, which should increase with every passing year and life style changes. Emergency corpus should allow you to sustain for emergencies like medical requirement, accidents, loss of pay/ job etc. One should keep at-least 6 months expenses in its emergency corpus. The monthly expense should include all liabilities like insurance premiums/ EMIs etc. You should keep it in liquid/money manager funds so that if you do not need it, it will grow at decent 6-8% returns as well as will be tax efficient. To avoid large draw downs from investments, make sure you have relevant adequate insurance of life/ health/ critical illness and for white goods extended warranties.

- Valuation of investments: One of the famous adages in the investment world is to “Buy Low, Sell High.” Though often I see people doing the reverse. You can gauge this by looking at the common queries on social media as well as in news-papers e.g. I have been doing SIP of Rs 2000 monthly for last 12 months in XXXX fund and at present I am in loss of Rs 1800, should I sell? Or My fund XXX is returning -18% annualized at present, is it better to sell and buy another? This happens because every-one focuses on their notional returns and do not understand the concept of volatility. IMO this is not the right reason to sell but you should do some selling/ Buying based on valuations in below manner:

- For Novice Investor: You should invest as per your risk-profile based asset allocations. Market will keep on gyrating between very high to very low, what you should do is to stick with your asset allocation and review it once or twice in a year. E.g. Person A has an asset allocation of 70 Debt & 30 Equity and in last 6-12 months equity has given fabulous returns of +50%, while debt has been consistent to give 8% returns. So now you have 75.6 Debt & 45 Equity (62.7% D & 37.3% Equity), you can either put new money in debt and do not invest in equity to balance it or sell some equity and transfer the money to debt. This way you will end up selling at High and vice versa situation buying at low.

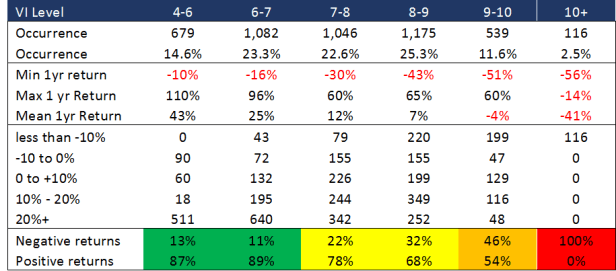

- For a Moderate & Experienced investor: Experienced investor should get more dynamic in their asset allocation. Those who like to be more active in their portfolio management then they should gauge the market valuations using publicly available metrics or having their own benchmarks like i follow valuation index. (Some of the Publicly available metrics as Motilal Oswal Valuation index (MOVI) or ICICI Pru Valuation Index.) If the indexes show you that markets are over-valued zone, then reduce your allocation to equity and vice versa in under-valued zone increase your equity allocation. I personally follow these along with market PE + PB based allocation as below, VI based valuation of 7-9 has been the most common zone, while every time it goes above 10+ it gets -ve returns on 1 yr forward basis. Therefore, If my asset allocation should be 50-50 than i reduce my equity holdings for 10+ zone to 25-30% and increase it in the below 7 zone (If it occurs) to 70-75%.

3. Tax Optimization: Very rarely I have seen people selling the MFs for the tax optimization. There are two main reason to sell your MFs for tax optimization. First to minimize your capital gain taxes and second to harvest the losses for tax benefits. This is not to be bothered by usual investor as it needs knowledge of taxation as well as monitoring the portfolio very closely. One should do it when the portfolio size is huge so that the tax gains become material.

- Minimizing Capital gains tax: Now in the new regime the equity capital gains are taxed if in a Financial year your realized capital gains are >Rs 1lac. If you have a decent equity portfolio of even 10Lacs gains beyond 10% will be taxable when you sell them. It is better churn your portfolio in intelligent manner so that every year you realize capital gains up to 1lac and reinvest the amount in next fund. Important to not keep money idle but move from one to another fund immediately. This will make sure your overall gains are taxed to minimum when you sell them completely as the purchase price is changing, and you are slowly realizing the gains. Similarly, in debt funds you can plan to invest in month of March so that if you stay invested for 3 years and a month you will get indexation benefit of 4 years. Therefore, churn your portfolio in a manner to minimize your taxable gains while no other cost occurs.

- Loss Harvesting: It is a common proverbial phrase that “When life throws a lemon, make lemonade”. In investing also, it might not be always possible that you see only gains in your portfolio there will be often scenarios when you see red in your portfolio. Instead of panicking and moving out to wait for a better time in the market. Just book your losses and make sure you reinvest at the same time. If the Capital loss is short term, you can adjust it against your short-term capital gains or long-term capital gains. And if the capital loss is long term then you can adjust it against long term capital gains only. Best part is that you do not need to adjust these losses in the same year, it can be carry forwarded up to next 8 years. Therefore, make sure you flag this in your tax filings every year till you adjust.

4. Wrong Purchases: People have an urge to buy the best fund, and in this process, they often end up having multiple funds in their portfolio. The number of funds goes beyond manageable, the max funds I have seen are 50+ funds while the simplest I have seen it just 2-3 funds. Another problem is created by the mentality of chasing past performance, so you buy the fund with best returns in the last 1 or 3 years. This has been shown by various studies and research that No fund stays as the best fund for consecutive multiple years. The best strategy is to stick with a fund with consistent record and which performs above average.

In Summary, if you are a new small investor make sure most of your selling is because of planned expenses or asset allocation re-balancing. Try to avoid distress sell and have your emergency corpus in place. Once you gain experience in managing your portfolio and it grows to a significant size, start utilizing Dynamic asset allocation. Look at 3 only when you have a large portfolio and too much time at your hand to monitor it rigorously. de-clutter your portfolio and stay within 7-10 funds at max unless you have a humongous portfolio, in that case also you might want to get into direct equity. If you have any other reasons to sell, it means that you have not bought the right investments as per your risk profile. Stick to your financial adviser to make the right choice of funds and investments and stick with it.

Do write to us your feedback, query and suggestions. Happy Investing!

Very valuable insight brother…thanks