“Reflection enables us to evaluate the experience, learn from mistakes, repeat successes, revise & plan.” Sherry Swain

First of all, Thanks for your love in 2020 which enabled me to continue writing and addressing your queries throughout the year. In 2020, we have not only added many subscribers and readers but the constant dialogue has also resulted in valuable friendship.

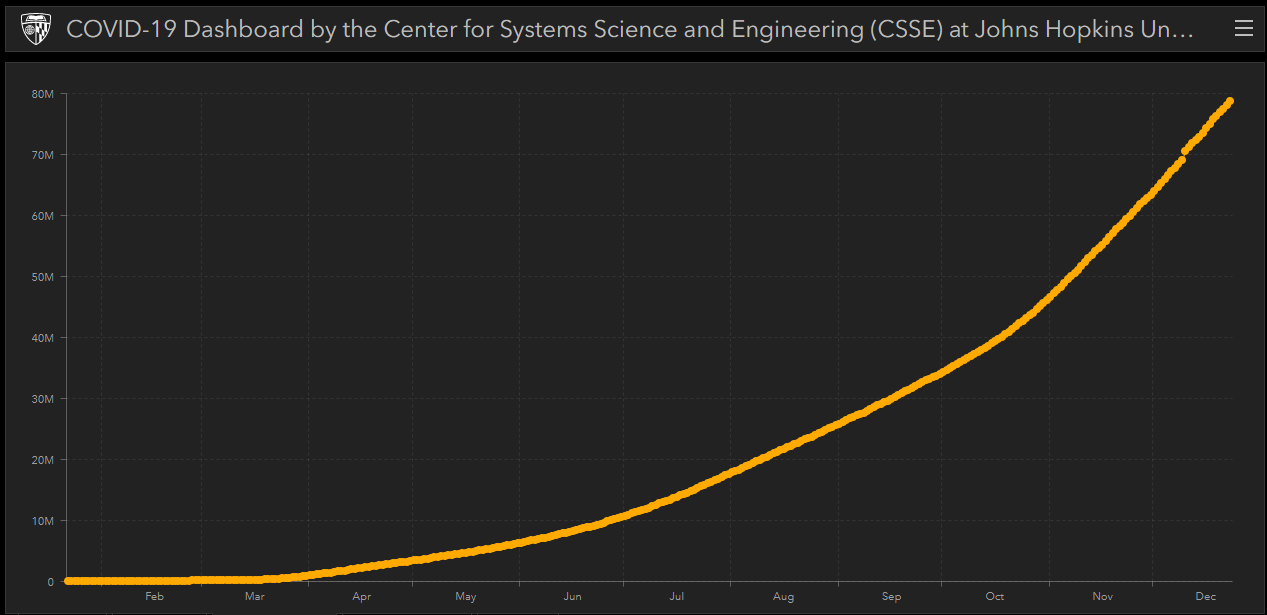

There are years with no action and there are days with year’s worth of action; 2020 has been a year full of actions such that a lot of us are exhausted. Typically I summarize the action on my investment journey but this year was different. We started Jan 2020 with the rising stress of Covid-19 in China but within a month most of Europe was struggling and then the whole world was impacted. In 2020, so far we have lost 1,700,000+ lives and counting. Even though the mortality rate from Covid-19 is <3%, The high speed of spread is testing the limit of medical care infrastructure across the globe as the total cases approach 80mm.

Apart from lives, a much larger population has seen an impact on their livelihoods either in form of job loss or salary cuts. During the last decade, the easy availability of the credit has encouraged people to spend their future earnings on today’s consumption and piled up debts in form of Home Loan, Vehicle loan, Personal loan, Education loan, Credit card loan etc. People were spending more on consumption by upgrading their TV Sets or Mobiles on easy EMIs. From FY 2010 to FY 2020, The amount of loan taken by individuals from Scheduled Commercial Banks have increased to >450% as per RBIs latest data.

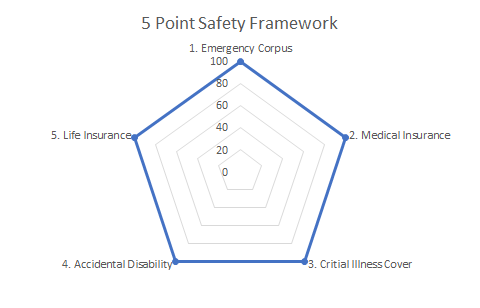

I touched on this aspect to remind few basics. Investing is a Long term game and to win the game it is paramount to stay invested and survive the large drawdowns. I am sure you know about Warren Buffet being one of the richest investor. Most people focuses on his ability to pick a great stock and multiply his wealth, though there has been limited spotlight on one of the biggest lever in his wealth; TIME. He started investing at a young age of 13 and has been compounding his wealth for last 75+ years. If you can invest INR 500 monthly at a 10% annual growth for 75 years, it will end up becoming >INR 10 Cr. Though most of us would fail to achieve so, mainly because of years like 2020 would force us to use our investments to consume in absence of regular income. Let me spend sometime on the five point framework to help you withstand such emergencies.

From the above 5 point safety framework for your investing portfolio, Emergency Corpus & Medical insurance are must for everyone. Life insurance is contingent on the list of people financially dependent on you vs. your accumulated corpus. Critical illness and Accidental Disability covers are beneficial but depends on your other priorities/ goals vs. disposable income. In 2021, I would build on these topics in detail so if you have not subscribed to our blog yet then do it now.

2020 Portfolio Performance Review

Coming back to the Investment journey in 2020 which has been quite successful, it has been the best year yet for absolute INR value gains as Portfolio returns. Hit the milestone first time that the return of Portfolio is equal to current annual expenses, Thanks to markets growth from the unprecedented fall to all time high. My current corpus had overshot the target corpus by +20%. Total corpus now stands at 27x+ of my annual expenses in India vs. 17x at the end of 2019. As my mutual fund portfolio is mostly built on 4 asset classes Short term Debt, Medium term Debt, Gold & Equities. Having restricted myself to just 10 mutual funds overall has helped me track/ monitor the changes successfully and this year has been quite lucky. Let me share some important points.

First is related to debt funds. After the withdrawal of my EPF, I had taken the sufficient position in Franklin UST scheme 30% of my financial portfolio in 2019. Though the increasing riskiness of the fund was keeping me on toes. When the Airtel & Vodafone recognized the large losses, I had started to pare my exposure which was reduced to 15% of portfolio by the time fund created the segregated portfolio for Vodafone exposure. I wrote about this in Nov 2019. Though the speed of redemptions had increased in the fund. After the close of FY 2019-20, In April I reviewed the fund again with conclusion to exit form the fund given I deem myself towards lower risk appetite. Franklin UST: Is it time to Exit? I exited the position completely & Next day the fund announced shutting down of scheme and money being locked down. This was Skill or Luck? I honestly don’t know but I am more inclined to call it luck. Re-emphasis on the learning that Return of Capital is Paramount vs. 1-2% additional return on Capital.

Secondly, The sale of debt fund with gains are eligible for tax. Over the last couple of years, I have been invested in the same equity fund which saw the -ve returns in the Feb/march carnage. This gave me the window of opportunity to replace my equity fund, if required. So I analyzed my HDFC Hybrid Equity fund in march, I sold my holdings to bring the tax liability back to zero. I had consciously decided again in favor of an active mutual fund vs. Index funds. This was at the time when the markets were falling with full force, I had the recommendation that it is time to buy now. below is the excerpt from my article Do’s & Don’ts during Market Panic. I had rapidly build the significant exposure on the equity side in march, which have paid handsomely so far.

If you are under invested in Equity, yes you should buy more now. If you have been sitting on cash due to concerns related to market overvaluations, yes you should buy more. If your earnings capacity is intact and your saving proportion increasing, yes you should buy more.

Lastly Gold, Obviously Gold was one of the biggest contributor of Portfolio growth in 2019. This year, Equity has displaced gold to the second position. If you remember that in early 2019/ Late 2018, I have been quite bullish on gold as asset class. I finally had put my thought in the article Gold to buy or Not to buy excerpt below of summary. In June 2020, When Gold has crossed it’s life time high then it was an indication of the breather, which I explained in Gold Hits Life time high! to suggest that still here is some juice left in gold rally but not outright.

The rolling 4 quarters demand of Gold by Central Bankers have been increasing sequentially over the 4 quarters. In current scenario if this trend continues then Gold supply is not enough to match it at least for next few years. Therefore, it makes sense to have more gold in your portfolio today vs last few years.

All in all, 2020 has been a great year for investments. All Asset classes have contributed to the growth.

2021 Outlook

If 2020 was a high growth year, 2021 is going to be more challenging. In last few years we have been targeting growth, now is the time to go on defensive and preserve the gains so far. Below lines from my last article, Indexes at all time high, I have started to book some profits. Even though the short term profits would be taxed but at least at a lower tax rate. The new money to equity would be least unless we have sharp downturn like 2020 again.

I am more inclined to suggest to be underweight on the equity as asset class. If your ideal Asset allocation to equity is 50%, you would be probably more prudent to keep only 30% allocation in current period.

After reaping the benefit of reducing interest rate cycle by generating double digit returns on debt funds with medium duration in last 5 years, Now is the time to slowly reduce the duration in my debt fund portfolio. So sticking to NRE FDs & Money Market funds. Though the interest rates might not start increasing in near future, it might be prudent to be aware of its possibility over next 3 years (Because debt fund holding of 3 yrs is required to make it tax friendly). Gold is going to be a buy on dips asset unless we approach the end of current pandemic, which would become the sign to start booking profits.

Let me repeat few learnings from investing over the last decade:

- If you are at the start of your career, Focus on increasing on your earnings and savings as that will form the main driver of portfolio growth

- Diversify across asset classes to have a balanced growth

- Reduce the number of funds / ETFs or Stocks in Portfolio to make it easy to manage

- If you want to get the full benefit of compounding, Make sure to have the five point safety net built for yourself

In the whole 2020, one thing which I definitely want to change is to reduce the number of transactions apart of my regular STPs/SIPs. Probably it was due to the dynamic nature of markets this year. Let me know, what do you guys feel about the various asset classes in 2021.

Wish you all a very happy new year & Prosperous 2021!