Over the last 3-4 years, I have simplified my portfolio and finally had only one equity fund in my core portfolio “HDFC Hybrid Eq Fund”. The exposure to this fund was pretty high and so were the losses in the recent fall. The losses were so tempting (yes tempting) that if i sell my holding, I could make my capital gains tax in the current FY to “0”. I had two options:

- Sell my current equity fund and then buy the same

- Sell my current equity fund and then buy a better available fund

Obviously, I didn’t want to cut my exposure to equity but increase it. I am sharing here my approach and analysis i did on historic data to pick the fund for Core portfolio. I decided to explore Option 2 because i knew, if i wont change the fund now then i might not change it for another 4-5 years due to lethargy. Also, This was one of the valid reasons to sell your funds.

Should i replace it with an Index fund?

I am sure, you would have heard the benefits of index funds. Lot of articles claim that the index funds are a good starting point including the “Mutual Fund Sahi Hai” campaign suggests Index fund as a starting point. Those who don’t know about index fund: “Index funds are passive funds, The mandate of Portfolio Manager is only to keep the holdings of various stocks in mirror fashion to the Index it is tracking. Two main indexes in India are NIFTY 50 or BSE SENSEX.” The usual benefit touted for index funds are lower expense ratios and no large under-performance vs the actual index. This was tempting and i thought to explore it. I picked the HDFC Index Nifty 50 fund, it has the long available history since the start of 2002 to compare with HDFC Hybrid Equity Fund.

Approach: I took the daily NAVs for both the funds since the start of Jul 17, 2002 to Mar 25, 2020. Calculated the rolling returns on a 5 yr basis for all possible 5 yr periods starting (for e.g. Jul 17, 2002 to Jul 16, 2007). I have also calculated the maximum draw downs for each of these 5 year period.

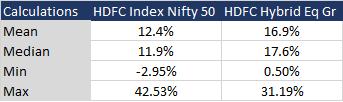

Results of Return Profile: There were 3000+ such rolling returns so to compare the results, i used the parameters like Geometric Mean of observations, Median of all observations, Minimum returns and Maximum returns. You will notice the out-performance of HDFC Hybrid Equity over the HDFC Index Nifty 50 fund. Though i might have to sacrifice some upside if it is going to be a bull market because the maximum possible return in historic data for HDFC Index Nifty 50 is higher vs the HDFC Hybrid Eq.

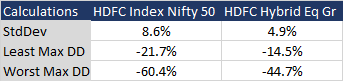

Results of Risk Profile: Some people will come back with the explanation that the out-performance is due to higher risk. So i also, looked into the risk profile using parameters like Standard deviation, max draw downs (MDD). I have calculated the MDD for each 5 yr time period to compare the lowest MDD or highest MDD among these 3000+ data points. You will notice the HDFC Hybrid Equity outperforms HDFC Index Nifty 50 on the Risk profile as well.

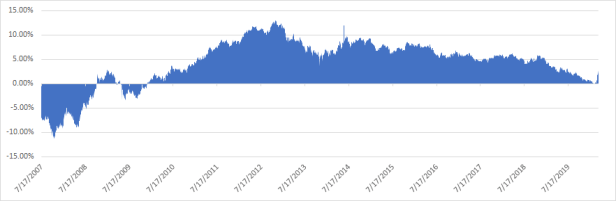

The last argument (which i also agree to an extent) is that as India market becomes more mature, Outperforming the index will be a challenge for active funds. Therefore, I looked at the history of these 5 yr returns to see the extent of out-performance (HDFC Hybrid Eq – HDFC Index Nifty 50). You will notice that HDFC Hybrid equity lagged the index returns in the initial phase, Then it continue to outperform for almost 10yrs.

The extent of out-performance has been deteriorating. Though it is still an out-performance with a lower MDD as well as volatility. Since, the data still points out that having an active fund is a better option, I ditched the Index fund again for couple of years.

Which Category of Active Fund should I Opt for?

This is another challenge that if i have to pick an active fund, Which category i should look for? In an article couple of years back, I highlighted the basics about how to build the Core & Satellite Portfolio. Over last year, I have also reviewed all the main categories of equity fund Aggressive Hybrid, Large Cap, Large & Mid Cap, Multi-cap etc, This has helped me get the foundation ready. Below is the approach i followed.

Approach: Let me start by saying that I did not consider Mid-cap funds for Core Portfolio as they are more risky & volatile and Small Cap funds are not for me. My heart was to move towards Kotak Standard Multi-cap fund after all they have ~30,000 Cr Assets under management in one fund. I picked the funds history from the start Sep 11, 2009 to Mar 18, 2020 and also compared it with the two best funds in each of the 4 categories which already reached by considering parameters like expense ratio/ turnover, AUM, Upside/Downside capture ratios etc. If the funds were started after Sep 2009, I did not considered them in the analysis. Here are the funds i compared against each other:

- Hybrid Aggressive: ICICI Pru Eq & Debt Fund/ HDFC Hybrid Eq

- Large Cap: ICICI Pru Bluechip/ Nippon Large Cap

- Large & Mid Cap: SBI Large & Mid Cap/ Canara Robeco Emerging Equities

- Multi-cap: Kotak Standard Multi-cap/ SBI Magnum Multicap

- Nifty Index 100 TRI (I don’t want to under-perform the Index so have to keep one Index)

Results of Return Profile: There were 1300+ such rolling returns so to compare the results, i used the same parameters Geometric Mean of observations, Median of all observations, Minimum returns and Maximum returns. You will notice that all of these funds have beaten the Nifty 100 TRI Index. This helped me build my confidence to stick with an active fund. Except Canara Robeco Emerging Equities, funds were having mean returns in range of 14-17% and it is also important to understand if the risk of these funds are quite different or same.

Results of Risk Profile: I looked into the risk profile using parameters like Standard deviation, max draw downs (MDD) in similar manner.

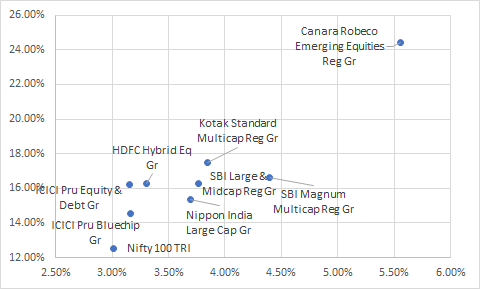

To make it easier for to visualize, i used the Risk vs Return chart for these funds, as below. You can now see that Canara Robeco was definitely most volatile in the lot, though its out-performance across funds were also astounding, For this fund, the volatility is an imperfect metrics because the lowest return (5.3%) for it was also the highest and so was the max return (35.3%).

There are only two funds which had lower risk vs HDFC Hybrid Eq, Though the returns of ICICI Pru Bluechip are lower vs HDFC Hybrid Eq so it is not worth considering. If i agree to take more risk, I should ask for higher returns and Kotak Standard Multi-cap does meet that criteria. After this exercise, I came to below possibilities:

- Reduce risk with similar returns: ICICI Pru Eq & Debt

- Take More risk & more returns: Kotak Standard Multi-cap or Canara Robeco Emerging Equities

As of today, I finally moved out of HDFC Hybrid Eq completely after an association of 10yrs+ and replaced it with one of these funds. The analysis here is not authoritative and obviously do not promise me future returns. It also do not cater to things like change in mandate or Fund manager etc etc. Though this gives me the peace of mind, That i am making a decision based on my analysis and understanding and it did help me improve my understanding of the investment options. Hope, i will be again in for long haul with >10yrs this time.

Happy Investing!!

Hi Sir,

if you could elaborate how to calculate rolling return and rolling risk step by step in separate article, It will be very helpful. Thanks

Sure Shiv, I will do the same.