As the Gold has moved >10% in last month, most of the people have started talking about gold. This is a renewed interest in Gold after almost a lull for past 5-6 years. There is a whole lot of new investors who have not seen the charm of holding gold, which pervades the old generation in India. There are still lot of communities in India which still continue their love for Gold.

Those, who are reading to find a way to increase their portfolio returns, can stop in here as Equity will continue to be the long-term out-performer across the asset classes. Then why are we even talking about Gold? It is to improve your portfolio return consistency and avoid the sleepless nights you get after seeing your portfolio in large losses (Read more at Asset Allocation). Today we will try to understand and address below questions. 1. Should we hold Gold as investment in our portfolio? If yes, How much? 2. Should we change the weight-age to gold, in the same manner as we do to equity due to valuation levels? If yes, when.

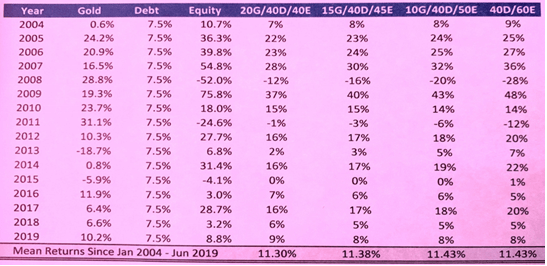

Let us analyse the data for last 15 years to see, if it makes sense to hold Gold in your portfolio. Below table gives us the colour in that aspect by comparing the returns of 4 sample portfolios as a buy & hold format over the last 15 years. 20G/ 40D / 40E means that portfolio consist of 20% Gold, 40% Debt and 40% Equity and similar for others. I have used the nifty returns as representative of equity returns and fixed return of 7.5% on our debt returns, which can be higher or lower depending on the avenue you opt for. What we can learn from this table.

Shortcomings of Gold:

- Since 2013, the Gold has been returning in lower single digits mostly and even negative returns

- Three times over the last 15 years, equity as an asset class returned negative over a year and only twice gold has returned +ve returns in those 3 instances

- Gold has returned -19% in 2013 and no rally in equity, if we would have bought gold in large portion, we would have got worst return in our portfolio

- There is no cash flow from Gold as an asset class, the only reason to buy will be expectation that the price of gold will rise in future/ continue to rise

- The more gold you hold, the lower will be returns over the long-term period

Benefits of Gold:

- It hedges the down-side, I wrote in details the importance of have better defence which can be read at (Defence wins championships). If you compare returns of portfolio 40D/ 60E vs 10G/ 40D & 50E, you will notice that not in even a single year the return of portfolio with gold outperforms. The Gold portfolio still matches the 15 years CAGR return of holding of equity & debt portfolio 11.43% each

- You will see the max drawdown in the E&D portfolio will be -28% vs -20% in G,E&D. If the Max draw down do not matter to you, (you can stomach large losses as well as volatility due to higher risk appetite) you can continue to hold your Equity & Debt portfolio or better just go 100% equity as that will fetch you extra 72bps return of 12.15% over the same period

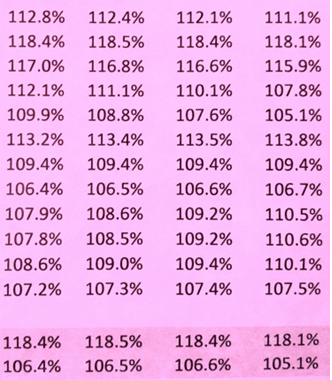

- If you look for the rolling 5-year returns, the E&D portfolio returns will range from 5.1% to 18.1% vs G,E&D portfolio returns of 6.6% to 18.4%. Apologies for missing headers, the portfolio returns as in same sequence as last table & last 2 rows reflect the Max & Min returns in each portfolios.

Limitations like what will happen if instead of buy & hold we are re-balancing or if we are investing regularly on a monthly basis. The limitations of this analysis are there but it can be used as a broadly fair assessment and should not change drastically. It will impact your overall returns and improve the volatility as well as max draw down (MDD) of your portfolio. 10% of the portfolio can/ should be in your overall portfolio.

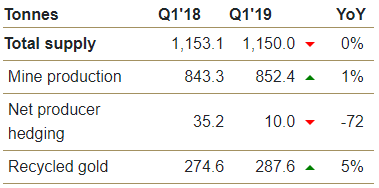

Now let me put down on my reasons why for last few months or a year I have been pushing people to consider Gold as an investment option because it follows the basic law of economics. If the supply is less than the demand, with increasing demand there will be rise in price of the product.

Supply constraints:

- Even when Gold can be found relatively easy underground, the quantities in which it is available, It is not suitable to be mined at industrial level

- Gold mining is hazardous and needs lot of planning, approvals and clearances before any firm can start mining it (Link)

- The lack of price action in yellow metal over last 5-6 years had discouraged lot of firm to spend additional money

These reasons have limited the supply of new gold in the world to the tune that currently for last 1 year it has been zero growth.

Demand variables:

- People in the Investment world are utilizing the availability of Gold ETFs and it is increasing the demand slowly as investment product. Even though small but at a rate of 50% it is not insignificant

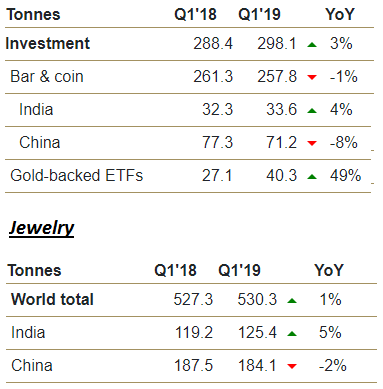

- Technology use of Gold have been small and constant so no major change in the variable but its use as Jewelry has been constant. Increased liquidity conditions help people increase the appetite to buy more gold Jewelry

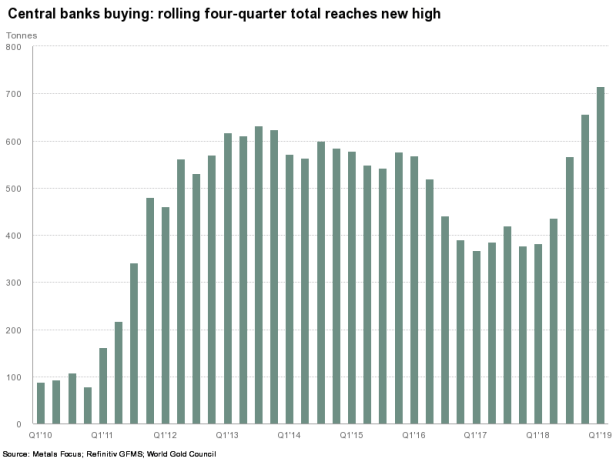

- Central Banks around the world have been the biggest driver this time around. As most banks keep $ as their reserve currency, the recent trade war of US with all major economies and Sanctions on Oil producing countries etc has not been perceived well with the world bankers and they are in process to reduce the $ reserves and replace it by Gold. (Read on RBI increasing Gold Reserves)

The rolling 4 quarters demand of Gold by Central Bankers have been increasing sequentially over the 4 quarters. In current scenario if this trend continues then Gold supply is not enough to match it at least for next few years. Therefore, it makes sense to have more gold in your portfolio today vs last few years. Also, to highlight the equity valuations are not cheap so expecting bumper returns in the coming few years without any major corrections will be difficult. (Read at Lessons from Nifty History)

Be informed and make your own call, based on your own judgement but don’t sit on the side-lines and not invest at all. Happy Investing!

——- Updated with 1H19 stats on the Gold market factors ———-

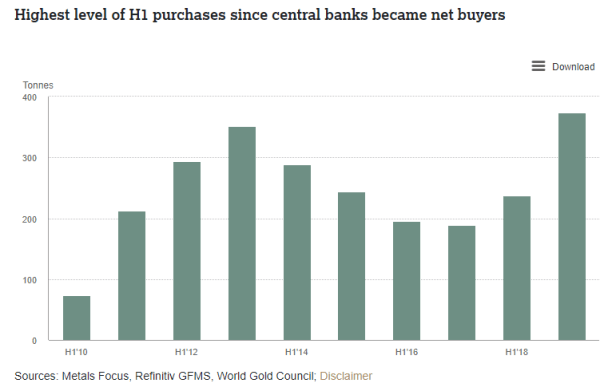

As we discussed earlier that the demand from central banks is driving the current gold prices and they are usually the first in participating the up cycle for gold. In 2Q 2019, Central banks bought 224t of gold which is 47% YoY. Poland itself increased their gold holding by 100t alone, more central banks are coming to gold markets to increase their gold reserves. In 1H 2019, total central bank buying in gold has been 374t up 57% and highest since 2010.

Central bank demand still geographically diverse. Nine central banks increased their gold reserves by at least a tonne in the first half of 2019. This continues the trend seen over recent quarters, where demand has been spread amongst a larger number of – primarily emerging market – central banks.

Russian gold reserves rose by 38.7t in Q2, bringing y-t-d net purchases to 94t, compared with 105.3t in H1 2018. Gold reserves stood at 2,207t at the end of June, equal to 19% of total reserves. Chinese gold reserves grew by 74t in H1. The volume of monthly net purchases increased marginally in Q2, bringing the monthly average for 2019 to 12.3t (11t in Q1). Turkey continued to increase gold reserves, up 60.6t in H1, while Kazakhstan added 24.9t to its gold reserves over the same period. Other central banks to increase their gold reserves by at least a tonne during H1 were: India (17.7t), Ecuador (10.6t), Colombia (6.1t) and the Kyrgyz Republic (2t).

The Central Bank of the Philippines announced at the end of May that it would begin purchasing gold from local small-scale miners. It is anticipated that buying could reach one million ounces a year, significantly higher than the current 20,000-30,000oz

What this means is that you still have play in the gold rally for next few months and quarters. Don’t go overboard with gold and don’t hurry to sell it either just hold it in right quantity as well as for right duration before re-balancing once in a year.