As markets are soaring to new highs, lot of people are raising questions like “Should i book my profits?“, “Should i stop my SIPs?” or “Is it good time to start SIPs, when markets are at all time high?” etc. I mentioned it in my last write up (How to Personalize your portfolio?) that it is quite essential to personalize your own portfolio. Unless you personalize the questions, often you will get the incorrect advise. Beautifully expressed in conversation:

“Would you tell me, please, which way i ought to go from here?”. “That depends a good deal on where you want to get to,” said the Cat. – Lewis Carroll, Alice’s adventures in wonderland

There are four main parameters to decide on the %allocation to equity in your portfolio. Once you have ranked/ scored these parameters for yourself, you put these in the calculator (Link) to get the equity allocation. Though let’s discuss how to rank or score ourselves on these parameters.

- Risk Capacity: Capacity refers to the risk/ volatility in portfolio, which one can withstand. It depends on lot of parameters like Job Security, number of dependents, Saving capacity, current portfolio size etc. If you have a stable job in Govt/ Public sector, your capacity is higher vs the person employed in highly competitive role like target based sales in private sector. Similarly, If you are living in nuclear family with your spouse and kids and both member (You and Spouse) are earning then your capacity is higher vs people who are sole earner in large joint families. Based on such parameters rank yourself from 0 to 5, where 5 being highest capacity and 0 being no risk capacity.

- Risk Appetite/ tolerance: This is different vs the capacity and solely depends on the individual behavior. There are people which have high capacity but their risk tolerance levels are low. This assessment should be done with the help of a professional or at least with someone who knows you personally well. This has a part of life discipline towards exercise or eating habits, attitude towards following traffic rules or voluntary tax compliance, reaching airports/ train stations on time/ before time or at last moment. Some people also ask questions related to market e.g if market falls by 40% in last 1 week what will you do? Nothing/ continue your investments as per plan/ stop your new investments/ buy more to average your purchase price etc. Again rank yourself from 0 to 5, 5 being highly disciplined vs 0 not at all.

- Time Horizon: Time is all mighty, as we say often. In investment world, also, it plays a crucial role. With time you not only get benefits of compounding but also have the chances to re-coupe your losses in full and gain handsomely for your investments. You might have heard the thumb rule like (100 – your age) should be your equity holding in your portfolio, as being the thumb rule it is quite crude. In my view you should look from the perspective of years to your main goals and what are your goals. If your goals are getting married, buying a car, going for a euro trip or buying a house then you are having goals in near future say 3-7 years time frame, even when you are young still you should keep equity exposure towards lower range. Similarly if your goals like retirement, marriage of children, children education etc, it means you have good number of years to fulfill those unless you are starting late. Again if you starting late and these goals are say 5-7 years far, less equity is suggested. So list your goals and chose the rank/ score based on average distance, 0 for <5years and 5 for 25+ years of time horizon.

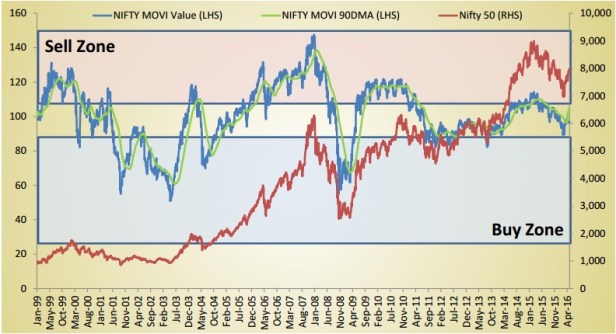

- Market Cycle: This is the section, which is more worrying to you in recent days. The advise, i recall from one of the best investment guru is that No one can predict the market move for tomorrow but still can put probability of its direction. Due to this one should never be 100% in equity market or 100% out of equity market. As we know everything works in cycles whether in economic cycle or business cycle or market cycle. Markets will soar new highs to fall back and touch the bottom to soar again, how long it stays at peak or bottom we do not know, we also do not know how fast they will fall or soar back. We can endlessly debate about the market valuation and it’s direction without any certainty. One option is to look for index available in market like, Motilal oswal valuation Index (Link) If MOVI is in 120+ zone, market is overvalued and MOVI of 80 & below indicates undervalued.

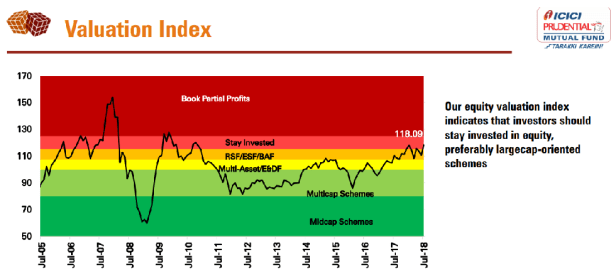

You can use Historical values of Nifty PE from the NSE website as well and decide the valuation zone to be overvalued (PE of 26+) vs undervalued (PE of 14 and below). You can also check the data provided by various AMCs to understand the valuation point of view e.g. ICICI Pru AMC publishes there Monthly market outlook includes the Market Valuation Index as below. (Link). Rank 5 for highly overvalued vs 0 for highly undervalued scenario.

Once you have successfully ranked/scored on these parameters, just punch in your scores on these parameters to know, How much equity should you hold in your portfolio (Link). This is again not 100% suggested method as on step 1 & 2, you need professional assessment so please speak with your financial adviser before making the final allocation by buying or selling. You should review this once in every year as your time horizon, Risk capacity etc will change with growth of your career as well as family events like marriage or child birth etc. Do not use it every alternate month to assess your allocations. Hope this helps and answers lot of your questions on equity Investments.

Read more on Mutual funds, Retirement Planning. Happy Investing!!