July this year has been not so good for Indian investors; Nifty 50 TRI was down -7.2% and Nifty Midcap 100 TRI was down -10.6%. The new comers in the Indian equity market who started their investment journey in last 2 years are not very well equipped with such falls in a month. The person opting for SIP in best mid and small cap funds since Jan 2018 are staring at -11.5% (HDFC Midcap – DG) and -16-17% (HDFC Small Cap – DG) XIRR returns. It is obvious to get scared and slowly that scare is turning into panic because the news headlines like below are not helping:

- Nifty Set to Post worst July in 17 years (Link)

“Business earnings continue to elude us and the commentary from consumer companies too don’t indicate that things might quickly mend in the coming quarters. If the slowdown persists into the festival season, FY20 too will have to be written off.”

-

Small & midcaps in a bear market; Nifty could head towards 10,300 by Dec 2019 (Link)

“There is more room for pain for the Indian bourses and we feel Nifty can reach levels of 10,300 -10,000 by December 2019. Though there will be short bounces and short-covering, the general medium-term trend will be downwards.”

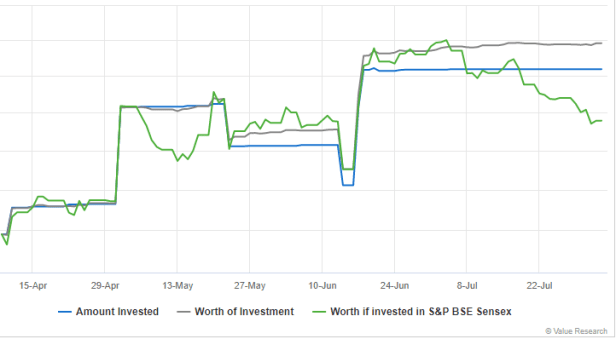

Lot of people now either want to exit from equity markets and don’t come back again as every-time they come come in equity markets the returns are abysmal. Though there are also another set of people who are learning to handle these situations. Today, i will share the examples of mistakes which most often people do and how to avoid it. if you will follow these five basics, you will be far better of in your financial journey on a long term basis. Now before i write down details, let me also share a proof that it works, below is the trend of my portfolio vs BSE Sensex over last 3 months. you can see how it reacted to market fall in May and now again in July.

#1 Not following the Asset allocation

Its not only me, but any person in financial investment field with some experience and knowledge will tell you that you should have a right asset allocation. I am just resonating that again, Though i do advise to follow the dynamic asset allocation to reduce the max draw downs in your portfolio as well as give you chance to outperform the market in the longer run. Why, how & when to do it have been written in details so not repeating it here, you can read Lessons from Nifty history & Benefits of Dynamic Asset Allocation.

#2 Not Buying the Equity market insurance

Anyone who have been following my posts on social media, I have been advocating to buy gold for last so many months. I know people will say it is a dead commodity, no industrial use except hedging the fear. The same is insurance (Hedging the fear). Think of it as insurance, It is still used as 2 reserve asset in most countries and when Dollar is not staying/ behaving the way market perceive it, everyone rushes to gold. I am not saying to buy large quantities of gold or if your family had tradition to hoard gold then avoid it but if you are from new generation who don’t see any value in gold ornaments, buy gold as portfolio hedge. Why and how much, again i have covered it few months back, please read Gold: To buy or not to buy!.

#3 Fund Hopping

Most of the people (including me probably a 9-10 yrs back) select the best fund based on last 1 yr performance and regret few months later as we ignored the caveat in mutual fund investment which says “Returns are subjected to market risk and past returns are not promised “. What you need to look for is the consistent performance and downside protection. I have got a much better handle on it and suggest you to go the same, Stick to your selected fund after careful analysis for at least 2-3 years of under-performance. Over a long period, most good funds will have similar return profile. How to review a fund and what all parameters to look for can be read at Category Review: Small Cap funds.

#4 Poor design of Core Portfolio

While chasing returns most people end up in mid/small cap oriented fund portfolio which has a poor core strength. One of the friends portfolio while reviewing i noticed that even when equity was only 30% of total portfolio but In equity portfolio he had 80% small cap, Mid cap or Sector funds (not to mention 14 of them). I am sure he is not the only with that issue and he was not first of my known with this issue. In a strong core portfolio you do not put small cap fund at all. It has to be good category debt (include your ppf/epf etc) and majority to be in Large cap/ Multi cap or Aggressive hybrid fund. More details on Core & Satellite portfolio.

#5 Not Re-balancing the Portfolio

Lastly, it is important to continue to buy low and sell high in the markets and one of the simple most philosophy advised is to re-balance your portfolio. Always review your portfolio 1-2 times in a year and re-balance it. If your asset allocation suggests to be 30 Equity and 70 Debt. Check it annually once at least and if it goes 35 E/ 65 D, then sell some equity and invest in debt or stop investing in equity for sometime and top up debt or vice-versa.

These 5 simple steps can make a huge difference in your financial life as well as emotional behavior toward finances. Hope you get awakened to correct your portfolio vs scared to get out of markets completely in this market correction. Markets will continue to gyrate between highs and lows, you need to make sure that your investments are optimal as well as continue to cater to your needs/ goals.

Happy Investing!!

If you find this information helpful, Don’t forget to like and subscribe to our blog.