“Good Judgement comes from experience, and a lot of that comes from bad judgement.” – Will Rogers

It is often said that your past experience shapes your future reactions, it can be best described with the proverbs like “Once bitten twice shy”. In the recent saga of NBFC’s default, liquidity squeeze and debt funds given large negative returns, I was completely unscathed from this fiasco even after heavily invested in this category of funds. This made me ponder on whether it was just pure luck or some actions/ judgement of mine which was build on past experience. After the careful analysis of my approach to investments made me realize that i am quite risk averse given my age, income and liability profile. I was able to pin it down to one of my past experience. I do believe that either you learn from your own mistakes or from someone else’s, I am sharing my experience so you can learn from the later than former.

It pertains to the period 1993-1999, the period of high growth and lot of corporate in India were raising the money in form of corporate deposits. They recruited the large number of distributors for commissions and returns promised were in north of 20% YoY. Most of you will instantly think that this was a poonzi scheme but lets think from the perspective of the person, who have limited financial experience so far and extra returns are always luring. (#As some of you were lured to invest in ULIPs/ Small Caps etc in hope to make >15-20% returns.)

One of my mom’s cousin approached her with this scheme to double the money in 3 years, she could not muster the courage to propose it to my father so from her pocket she decided to deposit 500 Rs in the scheme. After three years, when she got the cheque for 1,000 Rs and it makes her quite happy so finally she decided to put all her savings in that options increasing the exposure to 3,000 Rs. After next 3 years, she got the cheque of 6,000 Rs. Now she decided to tell my dad about it, convincing him that over last few years she doubled it twice. This time they together put down 12,000 Rs in this scheme, thinking this will be used for me & my elder brother’s college fees. Alas, this time they were not lucky and after a year the news that company is not returning the money to people whose deposits were due. We started to follow up with my uncle and initially he says it is temporary but later he started to escape us. The local branch of the company started to close down, and in one more year we started to get the news of cases piling up with the consumer court against company for fraud. the last deposit was in 1999 and by 2004 the cases have reached supreme court. Since i have been vigilant to follow financial news, luckily i spotted that in 2018, honorable SC has passed the judgement to redeem 70% of the principal to investors by liquidating the real estate assets seized from the company and as we had all the documents we finally received 8,400 Rs after 19 long years. I have graduated as well as post-graduated along with my brother and this amount is just not enough for even one months of expenses.

To double money in 3 years means 26% CAGR so If we would have kept churning our money in same investment, It would have been 9.68 lacs in 19 years. If we should have bought Nifty, it could have grown to 1.07 lacs and sticking to simple FD @8% could have returned 51,700 Rs. in reality instead of gaining the money with high return we end up receiving only 1/6th of the amount we could have got in fixed deposit in bank and less than 1% to what was promised rate of return. Obviously we blamed the company as well as that cousin of mom. Lastly we made another mistake that we became too conservative in our approach and all my fathers savings were happening in bank deposits, LIC policies and Post Office Saving’s scheme, which again was a mistake (Learning from our parents). Let us understand the mistakes we made and what to learn from this incident.

#1. Never trust your money to any person (including relatives) unless they possess the right qualification as well as experience. You might see a lot of distributors of financial services including MFs, Insurance etc are not very well qualified and mostly understand only the operational procedures of their craft vs understanding the craft and its nitty – gritties.

#2. Understand the basic tenant on which the returns are promised or provided, if you do not understand then do not invest. It is always better to be safe then sorry, we often blame others for our losses but most often it is our greed which drives us to take such investments and repent later. You will see at least few cases every year of one or the other poonzi schemes like chit funds scam in WB or Shariah investment scam in Karnataka.

#3. Credit Risk is real and have to be avoided if you can not assess it. You can either stay with safer investment options (How to build your debt fund portfolio) or Debt funds with high quality investments. For later, in simpler way just go to value-research-online to check the quality of bonds the fund hold. Do not check it only while investing but keep monitoring at least once in a quarter to be aware of the change. In general any Investments in AAA/ A1+ category of bonds is relatively safe.

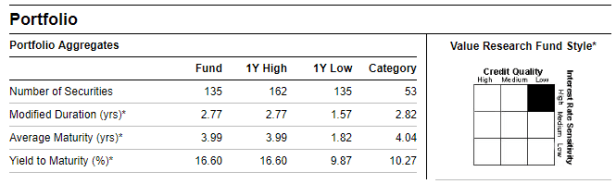

#4. If you do take exposure to credit risk, it has to be as per your risk appetite as well as risk capacity. It has to be an informed choice in search of return where you know the payout if your gamble pay’s off and what is the expected loss. for example if i buy the ABSL Medium term debt, which holds a low quality bonds due to exposure to subsidiaries of Essel group to an extent of 17%. My 1000 Rs investment might lose full 170 Rs exposure to lower credit bonds, which in turn leaves me with almost zero return after 2.77 years (Assuming remaining 830 rs will grow @8% to 1,027) or if the default does not happen i might get 1,530 Rs in return (YTM of 16.66% over 2.77 years). This is an educated gamble to be taken based on your risk appetite. (Debt fund investing)

#5. Interest rate risk is another component to understand while investing. Though it primarily is mark to market risk but it can affect your returns. If you know and can understand the interest rate cycles then you can buy bonds with Medium to long duration to generate extra mark to market returns in your portfolio. It is important to do it before the cycle starts vs doing in the middle of cycle as over a longer duration returns will converge to the YTM of the funds. (More to follow on this)

Lastly invest only in products and businesses, which you can understand because the risk comes from not knowing how to assess and manage risk. Hope this was a helpful learning for your investment journey.

Happy & Safe Investing!