“Remember to celebrate the milestones as you prepare for the road ahead.” – Nelson Mandela

In 2011, I first thought about the financial independence and wrote in Path to Financial Independence almost 10 years back. Even though my calculations of numbers were basic but I was thinking correctly about the issue & steps to resolve it. As the time passed, I get more and more organized as well as closer to my financial independence goal. Retire early or not, The Financial Independence continues to be main focus for me [#FIRE].

One major shortcoming of my basic calculations were the under appreciation for the impact of inflation, I am not talking about the normal reported inflation but the personal inflation. Common inflation would be 6-8% annually but personal inflation or what we call Lifestyle creep is much higher. In my bachelor life, My monthly expenses were 15-20k as most resources were funded by 4-5 people staying together. Post marriage they jumped by >100% as you need to bear the whole expenses at your end. There are other expenses, which increase due to upgrade of lifestyle like moving from bike to car, travelling by Flights vs. Trains etc. [Check my detailed article on Lifestyle inflation]

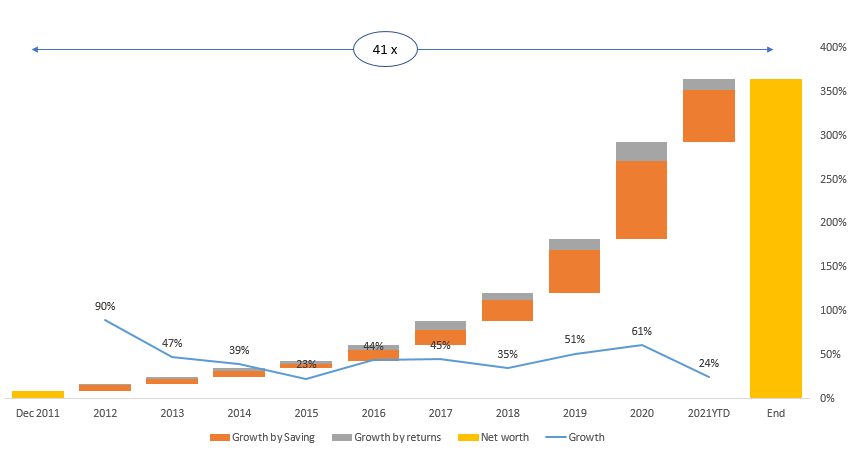

At the end of 2020 (Year in Review), I had accumulated the 27x portfolio [Currently ~33x] to my current expenses. By traditional benchmarks/ thumb rules, this milestone could be termed as Financial Independence milestone but as I explained in the analysis for a friend that it might not be sufficient for sure. In last 10years, my portfolio has grown by 41x at a compounded rate of growth of 47%. As I am slowing transitioning from the Phase 1 to Phase 2 of wealth cycle, The primary factor of the growth has been the increase in income & corresponding increase in savings. Now the growth in portfolio is increasingly driven by returns, 2020 growth by returns was > the overall absolute growth in any of the years from 2012-2017. Think & understand this point better as per your position in the wealth cycle.

In the last 10 years, There have been many lessons for improving the returns, which I plan to leverage in the next decade. The most important lesson among all is the concept of less is more. Earlier in my investing journey, I invested into various stocks & mutual funds. Tried chasing returns and did it successfully too. As your portfolio size start increasing, it is much more efficient to be a buy & hold investor. When you have higher churn rate in portfolio, you need to worry about the cost of transaction, exit loads, Tax implications. for e.g. you identify the opportunistic equity investment of 25% return in a year with INR 100k investment you book a profit of INR 25k next year (No capital gain tax) but if portfolio size is INR 1mm then INR 250k would mean INR 15k as capital gain tax. Higher churn also means more number of decisions to be taken, which in turn increases the probability of wrong calls. Below are the steps to be taken to improve your long term returns with lower churn:

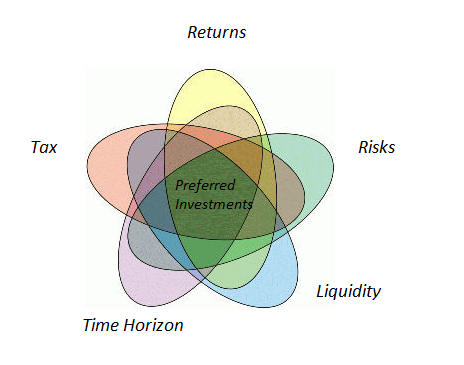

- The portfolio design should satisfy each of the five requirements in terms of returns, risks, liquidity, tax and your time horizon. It is a crime to invest your 1year ahead required money in equity like risky product as well as keeping all your 15-20 year far goal in 100% debt

- Buy right products in your core portfolio with relevant diversification as no one asset class would continue to be the lead return generating

- Diversification do not mean that you end up buying lots of funds or stocks. Simplification is as important as diversification.

- Do not sell your investments unless it meets one of the criteria flagged in when to sell your investments

I am quite hopeful, that the simple portfolio of just 5-6 funds can serve the most needs of an investor. As I am getting closer to my financial independence goal, I am helping more and more people to start their journey in more structured manner. I learned the process by hit & trial, started with zero inheritance and if I can do it, I am sure most of you can do it as well with little help & determination.

May this independence day brings you the aspiration to achieve your financial independence as well.

Happy Independence Day & Happy Investing!