Recently, I came across the news headline “Balanced advantage funds fail to deliver” in one of the leading financial daily paper published on Sep 3, 2019. Even though they tried to give both sides of the coin, they probably did some injustice to this fund/ fund category with some of the statements like below.

“Fund managers failed to move into debt and protect investors as equity markets floundered over the past year”

“The past three-year returns stand at 7.22% and 8.15% over the past five years, which essentially means that the returns were similar to what bank fixed deposits or a short-term debt funds give.“

Obviously, I won’t deny that they have to sell the news and sentiment which is prevailing in market (currently of bashing anything or everything to do with markets and economy). Let’s try to understand the details of this fund and see if we should chuck these funds out of our portfolio or accept them with open arms. I have an immense love towards this category and expressed the same in my article on the subject in July 2018 “Balanced Advantage funds: 5 reasons to invest in them“.

What are Balanced Advantage funds ?

As per SEBI Guideline, Balanced Advantage Investment scheme is an open ended dynamic asset allocation fund which can invest in equity/ debt which is managed dynamically. Therefore, in theory the % allocation to equity or Debt both can range form 0-100%. Though this creates a constant confusion for an investor as they have to keep monitoring the asset allocation to identify the tax treatment of return of the funds due to which most of the funds prefer to stick to the Pre-defined tax category as per their investment style.

ICICI Pru Balanced Advantage fund has been in category of equity funds which means they should have equity holding of 65%+ all the time, They can hedge some of the equity exposure using derivatives to reduce the net equity exposure but for practical purposes you can assume it to be in range of 50-100% equity exposure in most cases.

What should we expect in terms of their return and risk?

If we expect the long term average equity returns of 11% and debt returns of 7% in current scenario, the returns expected should be anywhere between 9% (50 Equity -50 Debt) to 11% (100% Equity – 0% Debt) on a long term basis. Since it has an equity component, the returns will keep on varying from period to period, though the volatility of the Balanced Advantage fund (range of returns/ variations) should be lower in these funds vs Pure equity schemes or Index.

How has ICICI Prudential Balanced Advantage Fund has performed so far?

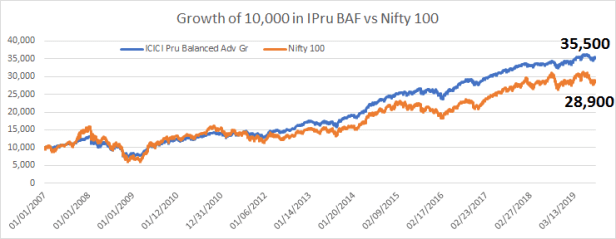

The fund was launched on 30 Dec, 2006. If we have invested in this fund Rs 10,000 on Jan 1, 2007 then today the amount invested would have grown to 35,500 or 3.55x in 12-13 years period vs 28,900 If the same money was invested in a pure equity index Nifty 100. (34,000 if we consider Nifty 100 TRI).

Source: Morning Star India & Edu-form

Obviously the fund does not promise to beat the equity index returns as their mandate but anyways it is great to see that they have beaten an equity index. Their benchmark index has been Crisil Hybrid 50-50 Moderate index and since inception the fund returns have been 10.45% vs 9.47% of the Index. (Source: Fund Fact sheet as of Aug 31, 2019)

If not the returns then what is the scheme mandate?

The scheme highlights are that it invests in both equity and debt. Aims to provide an opportunity for reasonable returns with relatively lower volatility. Seeks to provide investors an opportunity to benefit out of market volatility. Uses an in-house valuation model seeking to limit the downside risk during a falling market and aiming to capture growth opportunities in a rising market. (Source: Fund Page)

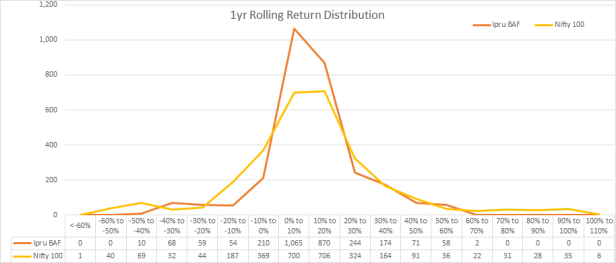

The main promise is around lowering the risk with still keeping the reasonable returns. The fund has successfully achieved the same over the years as per below chart.

The fund had a history of 12.5 years with 2,885 rolling 1 year returns and shows the fund has definitely delivered a superior risk management.

- Negative returns are observed only 14% times vs 26% times in Nifty 100

- Volatility of the 1yr rolling returns is 15.8% vs 24.6% of Nifty 100

- The worse 1yr return of -42.1% vs the -60.2% of Nifty 100 index

- The Max Drawdown in the fund over the last 12.5 years have been -45.2% vs -61.2% for the Nifty 100 index (To know more on Max Drawdown)

- The fund has a lower upside capture (62%) but the superior downside capture (44%) vs Nifty 100, The Upside/Downside Capture ratio of 1.4 helps it to deliver better risk adjusted returns

The fund has definitely performed on its promise and have stood against the test of time. To conclude:

- The argument of shifting 100% to debt is not practical mainly due to taxation if you compare it to FDs and Debt funds then please compare and contrast with the Hybrid Debt funds which are more inclined to generate alpha over Fixed Deposit returns.

- The return of 3.9% over last 1 yr is much better than that Nifty 100 return of -5%. The three year and 5 year returns have been closely tracking the Crisil Hybrid 50-50 Moderate index. Also, as an optimist in case of equity rally has a potential to move towards 9-10% while the way interest rates are going down, FD/Short term debt fund returns will be sub 7% range

- One more suggestion made in the article is to follow a 50-50 asset allocation, that is a good suggestion but don’t take the pain of re-balancing and taxation lightly as large swings in a short run in equity will need re-balancing more taxing on the wallet (as tax outgo) as well as time

I personally follow my own asset allocation and keep it managed at my end with active funds using dynamic asset allocation. Though, anytime if i want to step down and put my money to one fund category, it will be Balanced Advantage Fund. Therefore for all the new investors, i always suggest to build the core portfolio with this fund or start their equity investments with this fund category. The advice, which i will continue to render irrespective of how media portrays it. You can read my other fund selections in the Large Cap, Multi cap, Mid cap, Small Cap or Value fund category.

Don’t forget to leave your comment/ feedback. Happy investing!!