There is an ongoing debate for many years about investing in lump sum or in Parts over 6 to 12 months. I have met and heard people from both the camps and they have a pretty strong view on their own philosophy. Though in reality the answer always in between and depends on individual. Personal finance is always about personal choices and you should chose the option after understanding the options correctly vs just making decision based on perception. Today, I will try to put my perspective on the same topic but let us first understand the concept of XIRR, a method to calculate returns for intermittent investing in parts.

Rate of return is a simple concept, for a years if you invest INR 12,000 and after a year if you get INR 13,800 your rate of return is “(13800 / 12000) – 1” = 0.15 or 15%. Though if i invest the amount in a monthly fashion INR 1,000 every month, this creates a problem. In this scenario the money invested in first month stays invested for full 12 months and the money invested in second month stays invested for 11 months, similarly the money invested in 12th month stay invested for a month only. Therefore returns on each investments differ due to different period of investment.

Return on 1st installment = 1000 x 15% x 12/12 = 150; Return on 2nd installment = 1000 x 15% x 11/12 = 137.5; Return on 3rd installment = 1000 x 15% x 10/12 = 125; ..Return on 12th Installment = 1000 x 15% x 1/12 = 12.5. Overall Return = 150 + 137.5 + 125 + … + 12.5 = 860, So for same 15% return in this case the amount received will be INR 12,860. The absolute return here on overall investment is “(12860/12000)-1” = 0.072 or 7.2% but mathematically the true rate of return is 15%.

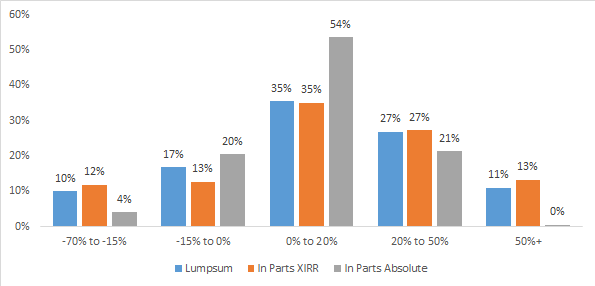

Now let’s come back to the original quest to understand “Should we invest lump sum or in Parts?”. To understand this, I ran the analysis on Nifty 50 TRI from Jan 2000 to Mar 2019 data. Case 1: when we invest INR 12,000 in one go and measured the returns over the first year, Case 2: when we invest INR 1,000 in 12 parts monthly and measure the returns after the first year in XIRR as well as Absolute terms. Why just 1st year returns, because after first year you will be 100% invested so any returns post that will be same in both scenario.

If you look at the first two bars that the Lump sum returns as well as XIRR returns are having similar distribution in each buckets for example 35% times the returns of lump sum investing is in range of 0% – 20% and so is for in parts investing in terms of XIRR. Therefore, there is no major difference of investing in lump sum or in Parts if you compare on XIRR. Though when you look in terms of absolute the story is quite different, there is only 4% chance to get <-15% returns vs 10% chance in terms of lump sum investing. This comes at the cost of giving up upside potential of generating returns >50% in lump sum 10% chance vs 0% chance to get such absolute returns while investing in parts.

What it means is that if you are having a aggressive risk profile and you do not need downside protection, then yes please go ahead to invest lump sum. Or you are an expert investor who can predict the market more accurately by active investing, then you can invest in lump sum and avoid the downside by predicting the market movements. For all other investors who do not know about market moves and are prudent to avoid downside, It is always suggest to invest your lump sum money over 6-12 monthly parts.

Please note this do not highlight that you should not do SIPs or regular monthly investing. This analysis is to be used only for your large sums like your Bonuses or withdrawal from insurance policies, PPFs/EPFs etc where the investment amount is quite high vs your regular monthly saving. The analysis here is for 100% equity investing using Nifty so you can still think of lump sum investing in funds where fund manager keeps juggling between asset classes like Multi Asset fund or Balanced advantage funds.

Lastly invest in the method you like, just understand the consequences and be ready for results as the gain as well as loss will be yours. You will be sad if loose more money but you will also be sad when your returns will be lower than the returns of lump sum investing. What will make you less sad, should be the correct and first question for yourself to finally decide about lump sum or investing in parts. Just don’t avoid investing.

Happy Investing!!

Also Read, Benefits of Diversification.

Hi Ramji,

What is your view on Brightcom Group.?

Can you share your analysis comment, it has a market cap of 300 cr and is engaged in Digital service and development of computer software services.

Request your opinion plz.

Regards Deep A Mukherjee

Hi Deep,

If I remember correctly then 6 months back we discussed Repro? How is that doing..

My comments on Brightcom will be similar, 1. It’s owner driven and not professionally looking for expansion/ 2. Mostly loss making in most of last quarters and 3. Lastly their liability is equal to Firms Market Cap.

Apologies if I don’t like such stocks, the Daily liquidity is merely 6lacs so again very easy to make large moves..