The Japanese concept of lean manufacturing includes the process to eliminate the waste, which are Muda, Mura & Muri (3M’s). Muda refers to process or activities that don’t add value. It increases the cost or delay the required results. Mura is a type of waste caused by lack of planning, which results in defects or fail to meet the requirements. Muri, is the 3rd category of waste, results due to over complicated process or unskilled executor/ worker. This concept is so powerful that it would be a crime for not to apply in managing your portfolio. Let me try to share some of the real life examples of such waste, I find in portfolios.

Muda/ Non Value add Component of Portfolio: A friend wanted to start investing in equity markets using mutual funds. He was suggested to start the SIP in “HDFC Retirement Savings – Equity (G)” for long term equity investments, which he did. Let’s understand the mandate & characteristics of this fund. “The total assets of the Equity Plan will be primarily invested in Equity and Equity related instruments (80-100%). However, the Equity Plan provides for flexibility to invest in debt instruments and money market instruments (0-20%)”.

It is benchmarked to Nifty 500 TRI which is justified given it will act as a multi-cap fund and the 0-20% exposure in debt is non value add and can be managed with other debt options separately. This fund has the expense ratio of 2.58%. Should we not replace the same with a pure Multi-cap fund from same AMC say HDFC Equity (G), which is also benchmarked to Nifty 500 TRI but with an expense ratio of 1.71%? If you argue about having debt component then HDFC Hybrid Equity (G) fund with 65-80% equity & Debt of 20-35% also with expense ratio of 1.71?

Now you might say, why I am so concerned about this 0.87% difference in the expense ratio? Let me help you visualize that over a long term 20yrs, INR 5,000 SIP @8% will create a corpus of 29.64lacs. If we reduce our returns by 0.87%, then @7.13% the accumulated corpus will only be 26.62lacs. The difference of INR 3 lacs, this is not too small. Imagine if SIP is for INR 50,000, the difference will be whopping INR 3million. Therefore, one must know what he is paying for the product/ service and the value he is getting out of that product/ service.

Mura/ Defects due to lack of planning: This is the most common one, Lot of people invest without a plan. They do not know there required asset allocation, they would not rebalance the portfolio based on market changes and target goal date and most importantly they would not know how to time the market, still most of them would want to do so. Let me explain it with one of the challenges faced by my friend.

He has been a long-term disciplined investor in HDFC Mid Cap Opportunities fund to accumulate the corpus for his kid’s marriage. In his 8 years of investment journey he garnered fabulous 22%+ XIRR, this has got in his head & created a bias that he can time the market and get huge returns. 2-3yrs prior to his goal, he skipped the advice to move his investment into debt products in step wise manner. He over smarted, thinking he would get at least 8-10% returns on his mid cap fund, hence he stopped his new investment and didn’t change the allocation towards debt fund. Unfortunately, that year Mid cap funds corrected by -11% and he saw the decline in his accumulated large corpus. Annual review has helped him correct his mistake and extra cash flow gave him cushion to overcome it, but you might not be that lucky.

There it is extremely important to stick to plan for your goals, if you are ahead of your goal then you can use the extra cash to create your tactical portfolio but DO NOT DEVIATE DRASTICALLY FROM A PLANNED CORE PORTFOLIO!

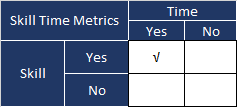

Muri/ Complex Portfolio or Lack of skill: Lot of people ask the question, Should I hire a financial planner? I think the below metrics can help you make that decision. Each task required certain amount of Skill and time to get done. If I have the skill to manage my portfolio but no time to do so, I would still struggle to manage my portfolio effectively. If I don’t have the skill but have time on hand, you can acquire the skill to manage the portfolio but progress will be slow and path will be long depending on your dedication to learn and execute effectively. For a successful DIY investing you should have both the Skill & the Time to do so. if both are missing, please hire a financial adviser without fail.

In my experience, I met lot of people who don’t have skill and spend lot of time in investing but end up losing without even noticing. For e.g buying lot of endowment policies (or large premium policies) for assured tax-free returns or Day trading in market and netting only sub 6% return post tax and transaction costs. If you do not know, how much effective overall return you made last year, it simply means you lack at least one of the required parameter. Address it before it’s too late.

Fix these wastage in your portfolio & you will gain much more than you expect along with peace of mind. Happy Investing!